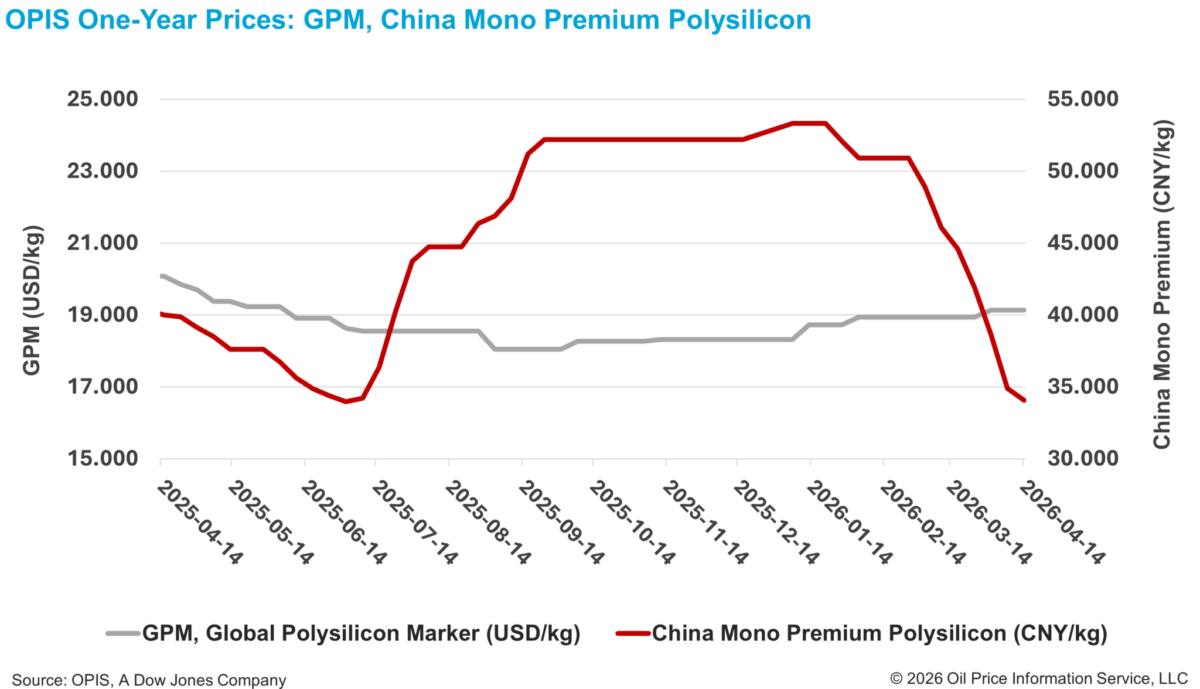

According to the OPIS Global Solar Markets Report released on April 14, the China Mono Premium—OPIS’ assessment for mono-grade polysilicon used in n-type ingot production—was down 2.36% week-on-week at CNY 34.071 ($4.99)/kg, or CNY 0.072/W.

Market insiders generally believe that the downward trend in polysilicon prices and continued inventory accumulation in China remain ongoing, with no clear signs of reversal at present.

One market participant noted that order volumes per transaction from major ingot and wafer manufacturers remain extremely limited, reflecting efforts to minimize inventory losses amid rapidly declining prices and further underscoring the current weakness in demand.

In response to prevailing market conditions, manufacturers have adopted measures such as initiating maintenance activities and further reducing operating rates. According to sources’ feedback, several polysilicon production bases in northwest regions have already implemented varying degrees of production cuts. Against this backdrop, the Silicon Branch of the China Nonferrous Metals Industry Association forecasts China’s April polysilicon output to fall about 8% from March.

However, one market participant noted that current operating levels are already constrained, with some manufacturers operating only a single production line, with that line running at a utilization rate of 50%–70%. Under such conditions, further significant reductions in operating rates are becoming increasingly difficult, the source added.

Another source indicated that major polysilicon manufacturers are currently able to cover only raw material and electricity costs at price levels of approximately CNY 31–32/kg, leaving limited room for further price declines. Nevertheless, smaller manufacturers facing loan repayment pressures may still be compelled to sell at lower prices, potentially exerting additional downward pressure on the market.

Earlier this month, the China Photovoltaic Industry Association (CPIA) issued a notice calling for the development of a standardized manufacturing cost model across the four key manufacturing segments, intended to improve cost transparency and help clarify the definition of non-compliant pricing practices. Industry views on the initiative remain divided, with some participants arguing that meaningful relief will depend less on the model itself than on whether it leads to effective measures for phasing out outdated production capacity.

Outside China, the fundamentals of the global polysilicon market remain largely unchanged, as the policy expected to have the most significant impact on the next phase of the market—namely the pending results of the U.S. Section 232 investigation—has yet to be implemented.

The Global Polysilicon Marker (GPM)—the OPIS benchmark for polysilicon produced outside China—was assessed at $19.138/kg, or $0.040/W, remaining unchanged from the previous week.

Market participants, however, have begun taking precautionary measures. Some downstream players with stable export channels to the U.S. have sought to secure long-term contracts for U.S.-produced polysilicon to ensure supply chain compliance. This trend has contributed to a

notable decline in spot trading activity, with current monthly spot transaction volumes reported to be limited to only a few hundred metric tons, according to market participants.

Spot trading of non-U.S. polysilicon has also remained subdued. A market observer noted that polysilicon from non-Chinese and non-U.S. sources currently faces a challenging position. Some key buyers prioritizing compliance are willing to pay significant premiums for U.S. polysilicon to ensure supply chain security. Meanwhile, certain players capable of rationalizing compliant supply chains in regions such as Africa and the Middle East are reportedly able to utilize traceable Chinese-produced polysilicon, thereby significantly reducing overall costs, the observer explained.

Industry insiders further indicated that a considerable portion of global non-U.S. polysilicon inventory is currently concentrated in Southeast Asia, primarily held under buyers with long-term contracts. However, downstream demand has remained insufficient to absorb these contracted volumes. According to sources, a manufacturer in Vietnam shut down part of its cell and module manufacturing facilities last month, while its remaining wafer, cell, and module integrated projects are operating at low production levels.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.