India’s cumulative tendered energy storage capacity grew from 6.8 GW in 2018 to 90.7 GW by 2025. Standalone energy storage system (ESS) tenders—which contract storage capacity without linking it to a specific renewable energy generation asset—accounted for more than 71% of the total ESS capacity tendered in 2025, with standalone battery energy storage system (BESS) projects comprising 60% of this capacity, according to a new report by JMK Research and Analytics and the Institute for Energy Economics and Financial Analysis (IEEFA).

“The surge in standalone storage tenders has coincided with declining battery prices and supportive policy measures such as the introduction and expansion of viability gap funding for standalone BESS projects,” says Vasu Mor, Research Associate at JMK Research and Analytics, and co-author of this report titled ‘Viability of standalone battery energy storage tariffs discovered in 2025’.

The report examines tariff outcomes observed in standalone BESS tenders in India, and examines the factors influencing tariff discovery, while evaluating economic viability under current market conditions, and mapping the near-term outlook for standalone energy storage deployment.

Among the 10.4 GW of standalone BESS capacity actually allocated in 2025, the 2-hour, 2-cycle configuration dominated. This type of tender configuration empowers energy offtakers to address both morning and evening peak demand windows within a single day.

“Since mid-2025, though, the 4-hour segment has been increasingly gaining prominence, as its higher single-cycle energy throughput is well suited to meet evening peak demand requirements,” says co-author Mouli Srivastava, Research Associate at JMK Research and Analytics.

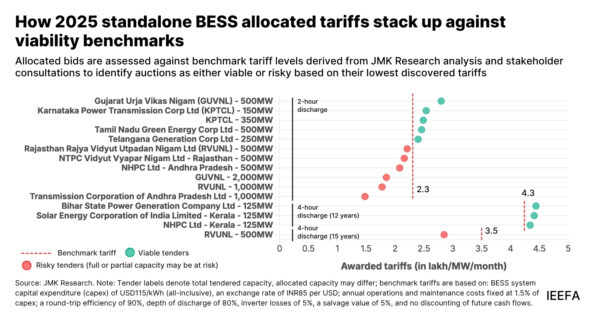

The report, however, flags tariff viability as a key concern for the 2025 standalone BESS bids. Tariffs fell sharply, with the lowest discovered tariff in the year reaching INR 1.48 lakh/megawatt/month ($1,576/MW/month) for 2-hour systems, against an indicative benchmark tariff of INR 2.3 lakh/MW/month ($2,448.95/MW/month) for 2025.

Nearly 75% of allocated 2-hour capacity now sits in the at-risk category, indicating a significant gap between discovered tariffs and actual project costs. Viable outcomes have largely been confined to early-stage, smaller-scale procurements through five state-led standalone BESS auctions in Karnataka, Tamil Nadu, Telangana, and Gujarat.

The report states that addressing this will require revisiting procurement frameworks, including introducing cost-reflective tariff floors, tightening eligibility criteria, and aligning auction framework with execution realities.

The report also evaluates the factors influencing the execution of allocated BESS capacity, focusing on battery cost trends, developer capabilities, and financing conditions. Execution risks in standalone BESS are expected to have broader implications for the sector. Implementation delays of up to 18 months may persist due to challenges related to financial closure, procurement and commissioning. Cost pressures at lower tariffs could also lead to compromised asset quality.

“Although the near-term challenges may lead to some project cancellations or delays, the eventual growth of ESS is inevitable. This momentum is already visible, with the majority of the around 1.8 gigawatt-hour (GWh) of grid-scale BESS capacity installed as of March 2026 having come online in the last six months of FY2026. Meanwhile, the aggressive bidding observed in 2025 is expected to gradually normalise as market participants recalibrate to execution realities,” says Prabhakar Sharma, Senior Consultant at JMK Research and Analytics, and a co-author of this report.

Overwhelming reliance on lithium-ion (Li-ion) technology has also exposed the Indian energy storage sector to global supply chain shocks, the report shows. Tendering agencies are likely to start focusing on alternative battery technologies with longer lifespans, higher salvage value, and lower exposure to supply-chain risks.

“Going ahead, the BESS technology landscape will be a diversified mix of storage technologies including Li-ion, flow batteries, sodium-ion etc. Their co-existence will be driven by different use cases, capacities, and tender designs, each offering distinct advantages in terms of duration, safety, lifecycle, and cost structure,” says Charith Konda, Energy Specialist, India Mobility and New Energy at IEEFA – South Asia, and a contributing author.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.