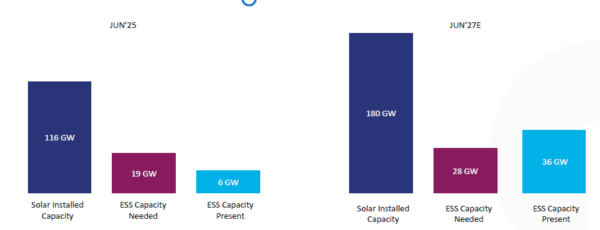

A recent report by SBICAPS projects that India will add 30 GW of energy storage capacity (battery storage, pumped storage, etc) through standalone and firm and dispatchable renewable energy (FDRE) projects by June 2027. This would bring the country’s total storage capacity to 36 GW—far exceeding the projected demand of around 24 GW, and possibly leading to oversupply.

“Presently, the storage capacity available is grossly below requirement considering Energy Storage Obligation (ESO) targets assigned. In the next two years, 30 GW of storage are expected to be added (standalone, FDRE, etc). This could lead to an oversupply as only 24 GW is expected to be needed by then,” states the report.

The report states that the excess capacities will remain reliant on energy arbitrage during times of peak mismatch on the exchange. Further, it expects the overall prices on exchange to drop gradually due to a combination of market coupling, electricity derivatives, and increasing storage, which will put higher cost players out of favour.

The report states that India can adopt China’s revenue stacking model combining income from capacity, ancillary services, and energy arbitrage for superior project returns. Currently, BESS revenues are dominated by capacity payments made by buying entities (typically Discoms) with/without intermediary at competitively bid tariff.

“The next stage of BESS project development in India would involve diversification of revenue sources beyond capacity charges through market based ancillary services monetisation mechanism with active participation from bodies others than SLDC/NLDC,” states the report.

Tendering in the Indian renewable energy sector remains focused on battery storage, with the first half of CY 2025 maintaining elevated level of standalone BESS and FDRE awards. Battery cost decreases have allowed for an increasing share of higher cycle, longer discharge projects at slim tariffs.

“Declining Li-ion costs now support more 4-hour tenders, with associated tariffs rivalling those of 2-hour projects—aligning with the typical evening peak duration,” states the report. “With a significant pipeline of under construction projects now built, the focus has shifted to execution.”

Execution bottlenecks

The report identifies land acquisition and getting transmission linkage (through a sequential two-stage process) as the key bottlenecks, which have stretched project completion timelines from 6-9 months to 18–24 months. Timely financial closure, viability gap funding (VGF) payments, and BEPSA execution also drive outcomes.

In the operational phase, risks related to technology performance and counterparty payment come into play. Faster-than-expected battery performance degradation and lower cycle life can impact project returns.

The report states that developers with proven execution capability, a strong counterparty mix, and low bid cancellations are best positioned to secure funding and emerge as sector leaders.

Upstream integration

The report states that upstream integration in India is in early stages for now, and global supply dynamic provides limited scope for domestication. Only a few battery cell makers globally have reported returns on equity (RoE) above 10%. The situation is not much better for precursors such as cathodes and anodes as well. While LFP remains relatively less crowded than NMC, supply remains high keeping capacity utilisation moderate.

Moreover, mastering cell chemistry is technologically intensive, with only a few companies such as CATL and BYD able to generate returns in a market plagued with low capacity utilization factor (CUF) across the ecosystem.

The report recommends ‘import to use’ strategy for the short term, with an eye on catching the next wave of battery technologies in the early stages.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

3 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.