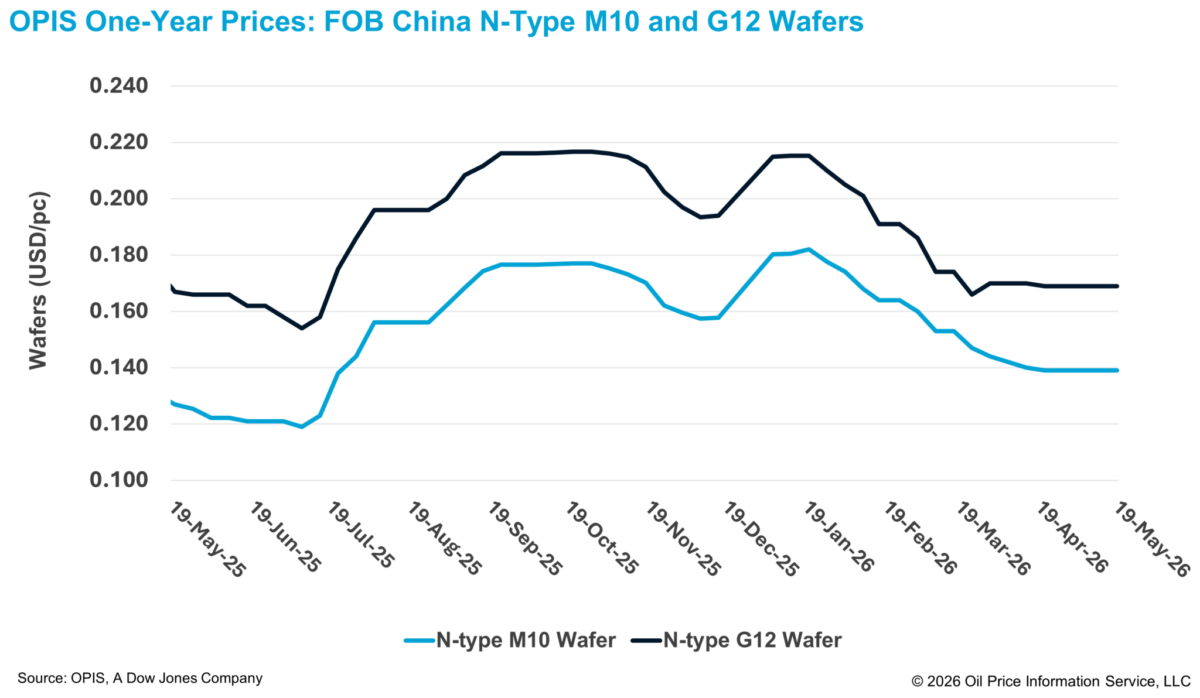

According to the OPIS Global Solar Markets Report released on May 19, Free-On-Board (FOB) China n-type M10 and G12 wafer prices remained unchanged week-on-week at $0.139 per piece and $0.169/pc, respectively.

Meanwhile, the newly launched FOB China n-type 210R wafer price assessment was assessed at $0.148/pc.

China wafer manufacturers have increased operating rates since May, leading to a corresponding rise in wafer inventories as downstream demand has yet to show meaningful improvement, according to market participants.

Market sources, however, emphasized that the recent increase in wafer operating rates and inventory accumulation should be viewed as a strategic move by manufacturers rather than a sign of worsening oversupply pressure in the weak market environment. Overall wafer inventory levels were reported to be fluctuating within the mid-20 GW range.

Wafer producers are currently utilizing polysilicon procured at price levels widely perceived by the market as near the bottom, thereby limiting the risk of further raw material devaluation, a market source noted. At the same time, manufacturers are intentionally building inventories in preparation for the traditionally stronger demand season expected toward the end of the third quarter.

The source added that the additional inventories are being accumulated with the expectation that they can be gradually sold at stable or potentially higher prices.

Other market observers maintained a more cautious outlook, noting that although demand from China’s domestic utility-scale solar projects has shown some improvement, the recovery remains limited. They warned that if the current slower-than-expected pace continues through the end of the second quarter, the possibility of another decline in wafer prices cannot be ruled out.

Another uncertainty on the demand side stems from the solar cell market. Industry participants noted that silver prices have risen again in recent weeks, adding to cost pressure for cell manufacturers.

With the wafer sector already facing the most severe margin compression across the photovoltaic supply chain, market sources said cell manufacturers will not be able to effectively offset these costs through lower wafer procurement prices.

As a result, some sources expect an increasing likelihood that some cell producers may reduce operating rates in the coming period to limit further losses.

In addition, market participants noted that module prices from a leading integrated manufacturer were seen declining further this week, which has continued to compress the sales price expectations of specialized cell manufacturers and further limited their production flexibility.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.