India’s target to achieve 500 GW of renewable energy capacity by 2030 and 60% non-fossil fuel energy by 2035, under its revised Nationally Determined Contributions (NDCs), will depend as much on debt financing structures as on policy or technology, according to a new report by the Institute for Energy Economics and Financial Analysis (IEEFA).

Titled “Financing the energy transition: A credit perspective on India’s power sector,” the report analyses eight major power generators: Adani Green Energy Ltd, Adani Power, JSW Energy Ltd, ReNew Power, NLC India Ltd, NTPC Ltd, SJVN Ltd, and Tata Power. Together, these account for approximately one-third of India’s installed capacity.

Annual investment requirements across renewables, storage, and transmission are expected to grow from around $68 billion by 2032 to $145 billion by 2035. Given the long operating life and capital intensity of renewable assets, long-tenor amortising debt will play a decisive role in determining the pace of transition.

“The power sector is already among the largest borrowers in India’s domestic debt markets, and this role will expand as investments accelerate. Transition planning is fundamentally a question of debt market planning,” said Kevin Leung, Sustainable Finance Analyst at IEEFA.

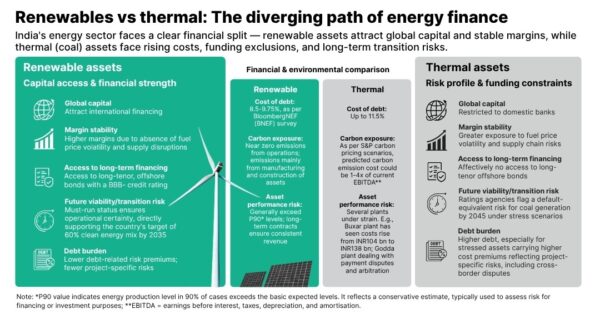

The report finds a clear and growing credit divergence between renewable and thermal assets. Renewable-focused utilities benefit from zero fuel costs, stronger margins, and better access to global capital markets. In contrast, thermal assets are increasingly excluded from international financing channels.

Notably, all outstanding USD-denominated bonds issued by Indian power utilities are linked to renewable or hydro assets. Tata Power’s offshore bond repayment in 2021 effectively marked the exit of thermal credit from that market.

“These are structural shifts in the economics of power generation, not cyclical changes,” said Soni Tiwari, Energy Finance Analyst at IEEFA.

The report also highlights uneven transition risks across companies. Financially constrained issuers face limited flexibility to decarbonise while also encountering restricted access to funding. In contrast, state-owned enterprises such as NTPC and SJVN benefit from implicit government support.

India’s corporate bond market, despite issuances exceeding $500 billion in 2025, remains shallow. The eight utilities studied rely on loans for nearly 80% of their debt, indicating significant untapped potential for bond financing.

Reliance on international capital also introduces vulnerabilities. During periods of geopolitical stress, foreign capital flows may reverse quickly, creating risks for transition financing. Strengthening domestic institutional investment—from pension funds, insurers, and provident funds—is therefore critical.

Among all utilities, NTPC is seen as central to unlocking transition finance. With approximately 17% of India’s installed capacity, majority government ownership (51.1%), and a sovereign-aligned credit rating, it is uniquely positioned to lead.

“NTPC’s INR 7 trillion capex plan through FY2032 makes it the most consequential capital allocator in the sector,” said Saurabh Trivedi, Lead Specialist at IEEFA.

Scaling renewable capacity can help deepen India’s debt markets while reducing climate-related systemic risks. With appropriate reforms, debt financing can evolve into a strategic lever for building a more resilient financial system and enabling sustainable economic growth.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.