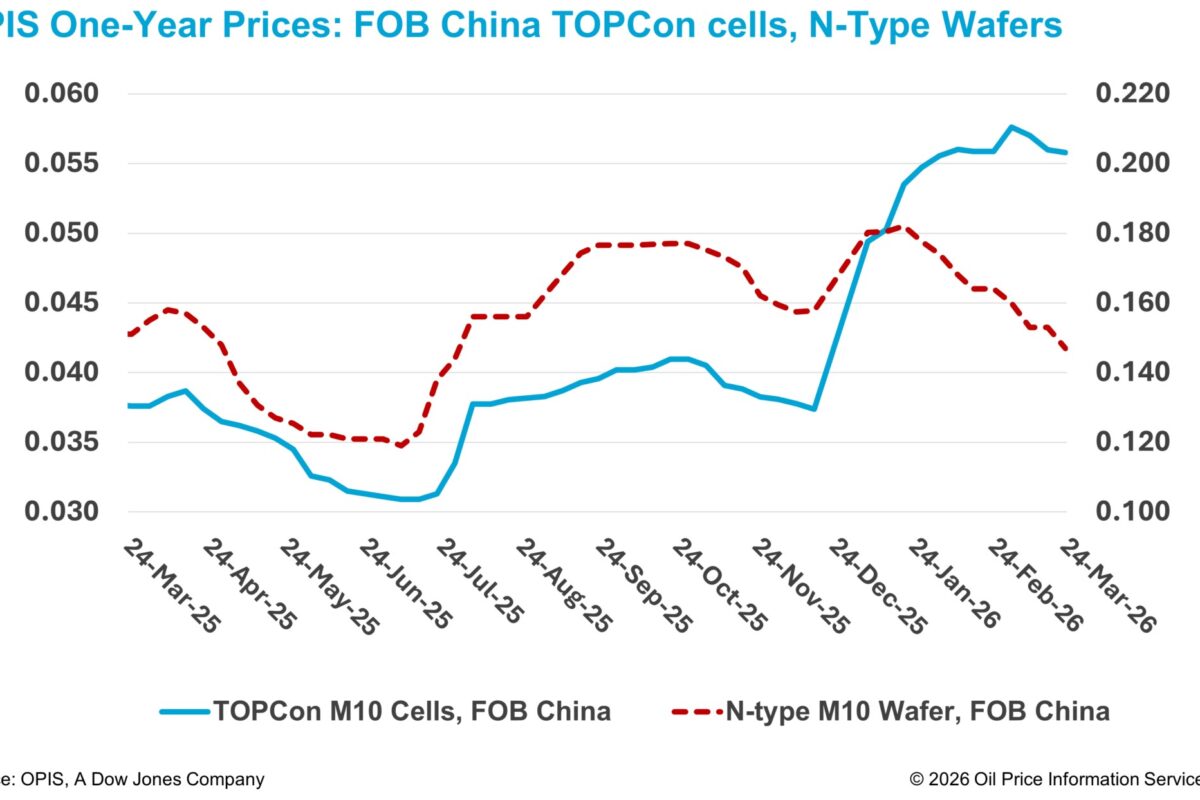

India’s battery storage landscape is undergoing a decisive transformation in 2025. Across utilities, regulators, and developers, BESS has moved beyond early-stage exploration and is increasingly recognized as an essential component for grid stability, renewable integration, and long-term energy planning.

- Storage moves from pilots to the middle of the grid-planning table

Over the past 18–24 months, storage has shifted from small pilots to multi-GWh tenders. Recent auctions from central and state utilities—including SECI’s hybrid and FDRE (firm and dispatchable renewable energy) bids, Rajasthan’s large standalone BESS tender, and emerging state-level procurements—clearly position storage as a mainstream asset class rather than an experiment.

At the same time, policymakers have started to hard-wire BESS into India’s long-term planning. CEA’s optimal generation mix studies indicate a need for tens of gigawatts of BESS capacity by 2029–30 to support the 500 GW non-fossil target.

From a supplier’s perspective, this is changing the nature of discussions with utilities and IPPs. We’re now talking about storage as an integral part of round-the-clock and peak-power portfolios, not as a separate “add-on” box at the substation fence.

This signals India’s transition from policy-driven trials to commercially meaningful, multi-GWh annual deployments over the next 3–5 years.

- Rapidly improving economics and smarter business models

The cost story is equally important. In just a couple of years, market-discovered prices in utility BESS tenders have fallen sharply, with the most recent auctions in Rajasthan setting new national benchmarks for storage charges per MW/month.

On the policy side, the central government’s Viability Gap Funding (VGF) scheme for BESS has been recalibrated as costs fall—the per-MWh support ceiling has been reduced significantly compared to early estimates, reflecting actual market-price movement.

For developers, this is pushing a shift towards:

- Revenue stacking – combining capacity, peak shifting, ancillary services, and sometimes behind-the-meter use.

- Hybrid portfolios – where the economics of solar + storage + occasionally wind are evaluated together, not in silos.

These price dynamics indicate a steady movement toward commercially viable storage even with reduced subsidies.

- Technology is maturing from “boxes” to fully integrated systems

Technologically, India has moved beyond asking, “Which battery chemistry?” to “How do we run this as a reliable, grid-interactive system for 15–20 years?”

A few clear directions are visible:

- LFP and ACC dominance at the front line of grid-scale deployments, driven by safety, cycle life, and economics.

- Multi-MW PCS platforms that are battery-technology independent, with DC voltages up to 1500 V and round-trip efficiencies in the high-90s.

- Fully integrated BESS – combining PCS, EMS, BMS, fire safety, thermal management, and communication in one engineered system rather than stitched-together components. Delta’s containerized BESS, for example, offers 150 kVA–5.5 MVA power with configurable 300 kWh–~5 MWh energy, grid-forming controls, and black-start capability for utility, C&I, and EV-infrastructure applications.

Equally, safety and reliability are now boardroom topics. That means designing for multi-level protection such as module-level BMS, integrated fire suppression, outdoor-rated enclosures and testing the whole system as a single product, not a collection of parts.

AI-enabled EMS, predictive analytics, and advanced fleet monitoring are emerging as key differentiators for performance and lifecycle optimization.

- Use-cases diversifying well beyond “renewables plus four-hour storage”

Grid-scale renewable integration will naturally stay the primary driver, but in 2025 we’re seeing BESS value being unlocked in multiple segments:

- Thermal-plant flexibility: India has begun piloting storage at coal plants to reduce ramping stress and better absorb mid-day solar, with NTPC leading large tenders at thermal sites.

- Rail and metro networks: Our own experience in deploying BESS with advanced-chemistry cells on the Kolkata Metro corridor – providing backup traction power and improving resilience – is a good example of non-traditional, high-reliability use cases.

- C&I and building-level storage: We increasingly see factories and commercial buildings using storage for peak shaving, diesel mitigation, and PV self-consumption where grid tariffs justify it.

- EV and data center ecosystems: High-power DC chargers and hyperscale data centers both place sharp, localised demands on the grid. Hybrid nodes that combine renewables, BESS and EV charging—supported by an EMS—are gaining traction, particularly as India’s EV and digital infrastructure expands.

From my perspective, this diversification is healthy. It spreads risk, builds operational experience across different duty cycles, and encourages more innovation in control algorithms and asset management.

This diversification reinforces BESS as a core component of national energy and infrastructure planning.

- “Make in India” and partnerships are reshaping the supply chain

Finally, you can’t talk about India’s BESS future without talking about localization. Between the national framework for energy storage, VGF support, and parallel programs for domestic cell manufacturing, policy clearly signals that storage should not be entirely import-dependent in the long run.

We see three big shifts here: Local manufacturing scale-up, co-development with Indian partners, and designing for Indian conditions, exporting globally.

In simple terms, storage is no longer just about adding batteries; it’s about building a resilient, intelligent infrastructure layer that supports everything from rural feeders and metros to hyperscale data centers and EV highways.

These policy and industry signals show that India sees storage as a long-term strategic sector requiring domestic value creation, not import dependency.

Looking ahead

If I had to summarize India’s BESS story in 2025, I’d put it this way:

- The “why” is settled – we know storage is essential to absorb 500 GW of non-fossil capacity reliably.

- The “how much” is clearer – multi-GWh targets and tenders give the industry a visibility it didn’t have two years ago.

- The “how exactly” is where innovation is exploding – in system design, business models, AI-driven EMS, and localized manufacturing.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.