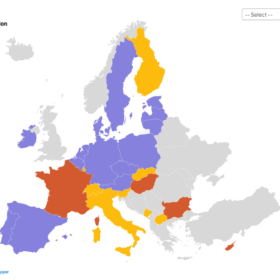

Europe creates map to locate available capacity in power grids

The new pan-European digital platform is designed to enhance transparency and improve access to information on the hosting capacity of European electricity grids, including both transmission and distribution networks.

India’s energy transition is becoming an economic story

Large Indian corporations are no longer adopting renewable energy solely to strengthen ESG positioning. Increasingly, renewable procurement is being driven by commercial considerations: lower long-term electricity costs, reduced exposure to fossil fuel volatility, and improving competitiveness in global markets that are rapidly introducing carbon-linked trade frameworks.

Why grid modernisation must precede energy transition targets

The future of energy is not merely renewable – it is intelligent, flexible, and resilient. This requires investment not only in generation assets, but also in transmission corridors, reactive compensation systems, digital controls, automation, and dependable high-voltage equipment.

Meeting the challenges of long life time PV on buildings

As Europe’s first generations of integrated PV systems age, researchers and industry actors are only beginning to explore the long-term realities of maintenance, compatibility and repair.

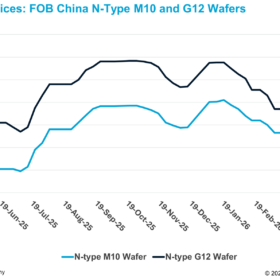

Chinese wafer producers build inventory ahead of expected Q3 demand recovery

In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

U.S. PV manufacturing capex could reach $7 billion in 2027 in breakout year for domestic supply-chain

Driven by multi-billion-dollar investments from the likes of Tesla and Corning, U.S. solar manufacturing capital expenditure is forecast to skyrocket 150% year-on-year to $7 billion in 2027, marking a massive breakout year as silicon-based technology eclipses thin-film spending and cements a domestic supply chain.

E-trucks: Unlocking the next frontier in India’s logistics transformation

As battery costs decline, charging networks mature, and financing models improve, e-trucks can move deeper into mainstream freight. India’s logistics transformation is no longer only about moving goods faster. It is about moving them with lower emissions, stronger energy security and better lifecycle economics.

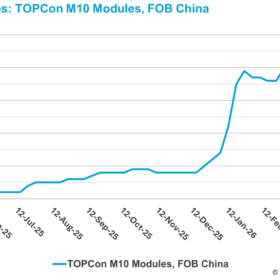

China TOPCon module prices hold steady as supplier price gap widens

In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

Solar approaches 3 TW, but the industry faces new challenges

Global solar PV capacity reached around 2,974 GW by end-2025, with nearly 698 GW added in 2025. The sector, however, is shifting from rapid deployment to integration challenges, as high penetration rates drive curtailment, storage demand, grid constraints, and evolving policy and market designs.

ARTsolar challenges local content compliance in South African solar tenders

A High Court in South Africa ordered the country’s Ministry of Mineral Resources and Energy to deliver full documentation relating to three solar tenders awarded in 2021 and 2022 to local solar manufacturer ARTsolar, after the company questioned if the preferred bidders had followed local content requirements for PV modules set out in the tenders. ARTsolar told pv magazine its legal team is currently reviewing the documentation it has received.