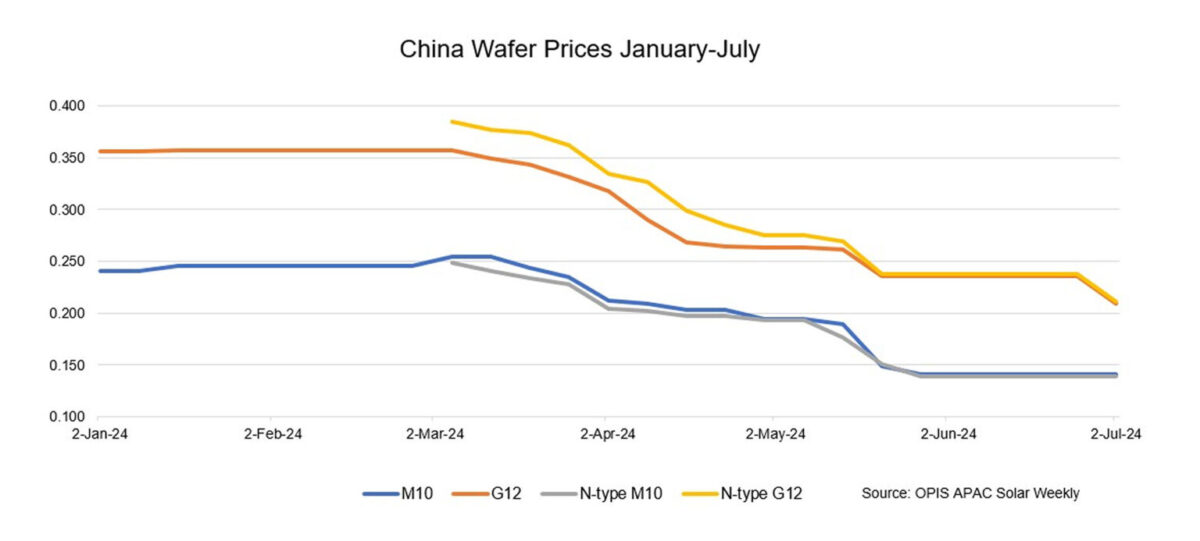

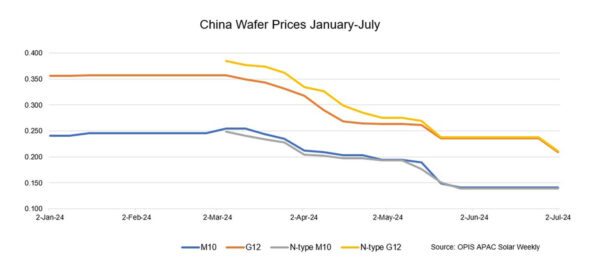

FOB China prices for M10 wafers have remained stable for the fifth consecutive week. Mono PERC M10 and n-type M10 wafer prices remained constant at $0.141 per piece (pc) and $0.139/pc, respectively.

FOB China prices for G12 wafers further declined this week. Mono PERC G12 and N-type G12 wafer prices decreased to $0.209/pc and $0.211/pc, respectively, representing week-to-week decreases of 11.44% and 11.34% compared to the previous week.

According to a wafer manufacturer who is still maintaining high operating rates at 90%, the cash flow condition and cost management—which here includes the company’s management and marketing expenses in addition to production costs—are crucial determinants of the viability of upstream polysilicon and wafer companies.

Industry insiders widely acknowledge that the Chinese wafer market has become saturated, with the next phase involving waiting for excess production capacity to exit. On the contrary, the establishment and growth of wafer production capacity outside of China are progressing vigorously.

A Chinese manufacturer promoting a wafer production project in the Middle East aims to commence production within two years, focusing initially on meeting local demand, according to a source from this company. Their secondary objective is to penetrate the US market, with plans to pivot to the European market should entry into the US market prove challenging, the source added.

Additionally, a European manufacturer, which ceased wafer production last year, recently announced plans to build a 5 GW ingot and wafer plant in the U.S. According to a source familiar with the matter, construction is slated to commence in late 2024, pending final approvals, necessary permits, and incentive agreements. Ingot and wafer production is expected to commence by 2026.

“We are also planning to bring wafer production back to Europe, provided that sufficiently attractive policy frameworks to support the solar industry are in place,” the source added. He further noted that the company is actively lobbying European policymakers to recognize the strategic importance of developing a solar value chain, advocating for the implementation of appropriate incentives and protective measures.

In terms of product technology, the current solar market is flourishing, impacting wafer makers’ operations and performance. A major wafer maker noted that the cost of wafers supplied to heterojunction (HJT) cell customers may be slightly higher compared to those used in other technology-driven cells.

The solar market has transitioned from an era driven primarily by advances in wafer technology to one where cell technology plays a central role, according to a source from an HJT cell producer.

A market observer agrees with this viewpoint, though with the belief that future technology trends will significantly impact wafer makers in turn. The industry is currently evaluating various technologies, including back contact (BC), tunnel oxide passivating contacts (TOPCon), HJT, and perovskite, to determine which will become prominent. One wafer maker is clearly geared towards BC technology, having recently acquired a BC technology specialist company, while another is focusing on larger wafer sizes. The question remains whether the market for larger modules, mainly used in utility-scale projects, will perform well this year.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.