From pv magazine USA

EnergyBin runs a business-to-business solar equipment commerce platform, selling secondary-market components for goods that are not sold via primary distribution channels. In its latest report, “PV Module Price Index for the Secondary Market”, it noted an increase in secondary market volume

, and an industry-wide decrease in module prices.

“Half-way through 2023, we began to see prices drop as the market sought to correct itself,” said Renee Kuehl, chief operations officer of EnergyBin. “Yet, we expect prices to continue to fluctuate as supply ebbs and flows. Therefore, it’s more imperative than ever to keep a watchful eye on prices.”

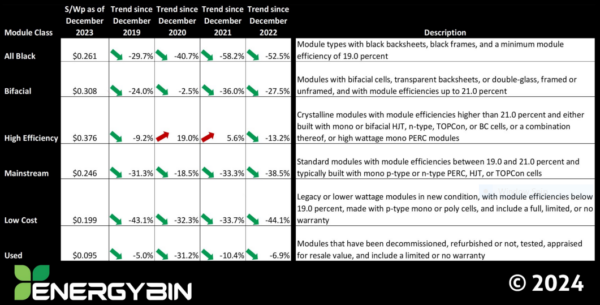

The most recent report shows data for module spot prices transacted in December 2023. Secondary market modules traded on EnergyBin traded at $0.261/W for all black modules, high-efficiency modules fetched a price of $0.376/W, mainstream modules $0.246/W, low-cost modules $0.199/W, and used modules averaged $0.095/W.

Mainstream modules are defined as standard modules with efficiencies between 19% and 21% and typically built with mono p-type or n-type PERC, HJT, or TOPCon cells. This category of modules has decreased in price 38.5% year-over-year since December 2022. More than 80% of the modules traded on EnergyBin in 2023 had efficiencies of 19% or greater. “Low-cost” modules are legacy or lower wattage modules in new condition with efficiencies at or below, and these modules have decreased 44.1% year on year.

Image: EnergyBin

EnergyBin’s report is based on the sale of over 5.4 million solar modules, with several transactions exceeding 15,000 units. Its largest lot sale was 65,520 modules. The company noted a 17% increase year-over-year in total count of modules sold and 27% growth in the MW capacity of the total sale of modules.

Solar modules have several different ways of reaching the secondary market. This can include remarketed products that primary buyers aren’t purchasing, including clearance, close-outs, surplus, and miscellaneous one-off sales. Modules may also enter the market via asset liquidations from acquisitions or bankruptcies, products for resale as a result of cancelled projects, delays, or downsizes. EnergyBin also sells products that are used, refurbished, or have no manufacturer warranty.

Buyers engage in the secondary market to efficiently request quotes from multiple suppliers, access bulk order discount, or locate hardware that primary vendors do not carry or do not have in stock. Secondary markets often give buyers the chance to secure low costs for equipment.

The report noted that U.S. module pricing is about $0.10 to $0.15 per watt higher than global prices due to Section 201 and AD/CVD tariffs and other administration costs like customs bonding.

EnergyBin said the most sought-after brands in 2023 were Canadian Solar, Jinko, REC, JA Solar, Qcells, and Longi. The most common module format are 144-cell “mid-size” commercial modules that typically measure around 82 inches by 41 inches and are compatible with microinverters and power optimizers.

“I have urged some module manufacturers to maintain their production of 450 W to 500 W mid-sized modules rather than producing the 500 W to 600 W modules,” said Paul Kriedermacher, owner and engineer of commercial and industrial solar installer MinnSolar Inc. “Ideally, we’d like to see a module in that range with its junction box positioned at the end of the module to provide superior wire management that meets NEC screening requirements for these types of systems.”

The report also noted high demand for U.S.-made solar modules, which on average fetched 40% to 45% higher prices than imports, excluding those from Western Europe. Tax credit bonuses allocated for solar projects using domestic content are driving the demand for U.S.-made components.

Looking ahead, EnergyBin expects prices to continue to fluctuate through 2023 as new players enter the market and the solar industry transitions from p-type to n-type cell technology.

“Like the primary market, the secondary market is not just about hardware,” said EnergyBin. “Much of the market’s success lies in value-added services that seek to maximize the performance and lifespan of PV assets and provide responsible disposal solutions for end-of-life material. Companies that add services, including inspection, testing, repair, remarketing, and recycling to their business models will increase profits over time while contributing to a sustainable circular economy.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.