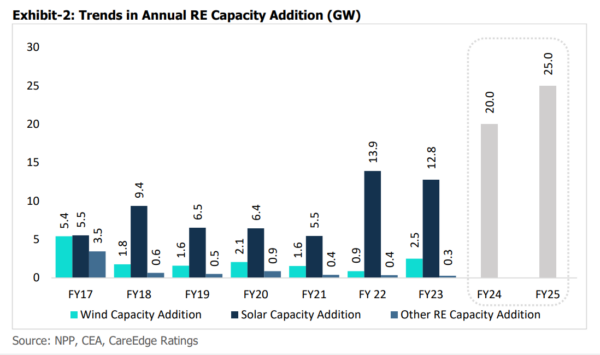

A new report by CareEdge Ratings expects India to install 45 GW of new renewable energy capacity over the next two fiscals.

The analysts expect the nation to install around 20 GW of renewable energy capacity in FY 2024, led by the solar sub-segment. This will be followed by the installation of over 25 GW in FY 2025—thus leading to cumulative addition of 45 GW over the next two fiscals.

Currently, India has a healthy pipeline of over 55 GW assets under development, which will drive significant capacity addition till FY 2025. Further, the indicative bidding trajectory of 50 GW annually will lead to capacity additions.

The analysts said India installed cumulative renewable energy (RE) capacity of around 125 GW as of March 31, 2023. Solar capacity leads the way at 67 GW, followed by wind capacity at 43 GW.

The nation’s annual RE installations must exceed 40 GW to achieve the 2030 target of 500 GW capacity through non-fossil fuel sources with segment-wise targets of 280 GW for solar and 140 GW for wind. To facilitate this, the government has committed to the bidding of around 50 GW RE capacity annually for the next five years through central renewable energy implementing agencies such as NTPC, Solar Energy Corp. of India (SECI), NHPC, and SJVN. The trajectory for FY 2024 includes 10 GW of wind capacity and 40 GW collectively from solar, hybrid, and storage-based capacity.

The analysts said one-year relaxation for the approved list of module manufacturers (ALMM) order is a positive for 25+ GW of unimplemented solar capacity awarded at a tariff of less than INR 2.5 ($0.030)/kWh.

The decline in module prices also bodes well for the implementation of over 25 GW of unimplemented solar capacity.

“Although the non-tariff barrier of ALMM has been put on hold for a temporary period, developers continue to be affected by tariff-related barriers, such as the basic customs duty on cells (25%) and modules (40%), which restrict their returns. Despite the external macro-environment being beyond the government’s complete control, recent developments have shown a positive trend, with module prices declining to 21-22 cents per watt compared to the range of 28-30 cents per watt between October 2021 and December 2022,” said the analysts.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.