From pv magazine Global

In February 2021, US President Joe Biden issued an Executive Order calling for the establishment of resilient American supply chains intended to, in part, advance the fight against climate change. To achieve the current goal of 100% clean electricity by 2035, the US Department of Energy (DOE) estimates that solar energy would need to grow from 4% of electricity supply today to 40%.

This kind of growth will increase the demand for everything along the solar supply chain, from polysilicon through to modules. With both goals in parallel, the desire to foster a domestic supply chain and the necessity to ramp up renewables, the question begs: to what extent can the domestic US solar supply chain be expanded to meet clean energy goals?

China’s dominance

The solar supply chain has long been reliant on products from China, or from Chinese subsidiaries in Southeast Asia. As of 2021, China was responsible for manufacturing a dominant share of the solar supply chain, according to statistics from the US Department of Energy.

As a manufacturer, China has a mixed reputation in terms of its environmental and social credentials, as much of its electricity generation utilizes coal, and there have been credible accusations of human rights violations in a region where some solar manufacturing is located. Given this and various other trade disputes, the United States has also had an unpredictable and somewhat fraught trade relationship with China.

Securing a domestic supply chain to support the United States’ clean energy transition has become increasingly important since the start of the global energy crisis caused by Russia’s invasion of Ukraine. At the Sydney Energy Forum in July, US Energy Secretary Jennifer Granholm cautioned against “relying too much on one entity for our source of fuel.”

Granholm described the transition to renewables as “the greatest peace plan of all” because countries cannot be “held hostage” over access to the sun or wind. “They have not ever been weaponized, nor will they be,” she said.

Polysilicon problem

The solar industry is experiencing a critical shortage in polysilicon and prices have hit highs not seen since 2011, due in part to a major manufacturer in Xinjiang closing unexpectedly for repairs. The Xinjiang region in western China is the origin of nearly 50% of the world’s supply of polysilicon, and it is currently under scrutiny for allegations of forced labor.

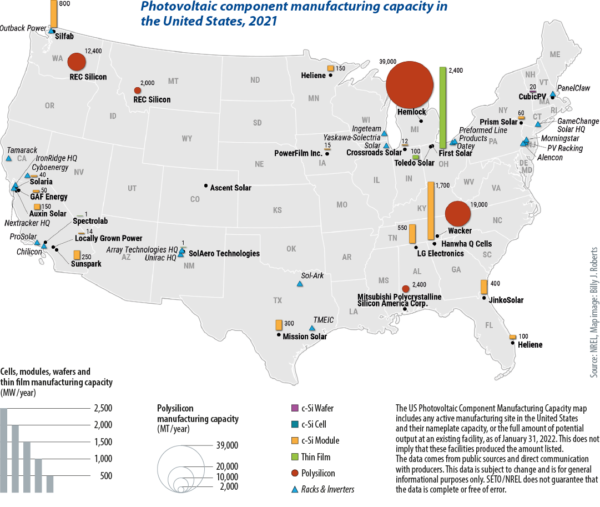

The United States has domestic polysilicon production capacity; however, as of 2021 it was not being used for solar applications – but that may be changing. In March 2022, Hanwha Solutions announced that it was increasing efforts to supply customers with “Made-in-America” products.

Hanwha, the South Korean company that owns module maker Q Cells, launched this effort by becoming the largest shareholder REC Silicon, a major US-based manufacturer of polysilicon. Following its initial $160 million acquisition to take a 16.67% stake in REC Silicon in January 2022, Hanwha is acquiring an additional 4.67% stake from Aker Horizons in a deal valued at approximately $44 million. This investment will help American manufacturers secure the raw material critical to the solar supply chain.

While developments in polysilicon production are promising, crystalline silicon ingot, wafer, and cell production in the United States remains nonexistent. However, the United States is home to a small but growing number of solar module manufacturers.

Q Cells and JinkoSolar, both with manufacturing operations in China, have established operations in the United States. With its headquarters in Switzerland and production in Germany, Meyer Burger announced in December 2021 its intention to set up a module assembly facility in Goodyear, Arizona. Mission Solar, and Solaria are also crystalline silicon PV manufacturers that originated and operate in the United States. And Silfab produces modules in Washington and Toronto, Canada.

Racking, tracking

Mounting structures are composed mostly of heavy steel components, and while the steel is relatively inexpensive, shipping costs can make up a significant portion of the finished product. Therefore, it is most cost effective to source products near to where they will be used. Most of the leading racking companies in the US marketplace manufacture exclusively in the U.S. including Unirac, PV Racking, ProSolar, Quick Mount PV, Oatey, DPW Solar, and Tamarack Solar. IronRidge manufactures, in part, in the United States.

The two largest tracker vendors, both globally and in the United States, are the US firms Nextracker and Array Technologies – collectively representing 70% of 2020 U.S. tracker shipments, and 46% of 2020 global tracker shipments. Based in San Jose, California, Nextracker was originally a U.S. company, but was acquired in 2015 by Singapore-based Flex.

Power electronics

Inverters and power electronics are an example of where the global supply chain comes into play, as many components are typically manufactured in separate locations around the world. According to the DOE’s “Solar Photovoltaic Supply Chain Deep Dive Assessment,” published in February 2022, most of the European and Chinese companies manufacture domestically, but many inverter manufacturers produce products abroad, particularly those that manufacture module level-power electronics (MLPE).

Among MLPE producers, SolarEdge, headquartered in Israel, has production facilities in Hungary, China, and Vietnam. The second leading MLPE producer, Enphase, is headquartered in the United States, and has production facilities in China and Mexico.

Interestingly, the inverter supply chain varies by inverter type, with U.S. utility-scale inverters largely supplied by European and Japanese companies, and residential inverters coming from U.S. and a large number of other foreign countries.

More American-made

A recent Wood Mackenzie report estimated that with supportive policies, an additional 20 GW of US manufacturing could be added. The Inflation Reduction Act (IRA) of 2022 was signed into law in August and is the most significant clean energy legislation in US history.

The IRA contains $370 billion in spending for renewable energy and climate measures, including over $60 billion for domestic manufacturing across the clean energy supply chain, which includes clean energy vehicles. The bill provides the support needed to achieve American manufacturing independence and clean energy security as we move toward a carbon-free future.

Thin-film PV production

Thin-film PV production

Cadmium tellurium (CdTe) thin-film PV technology was developed in the United States and makes up about 20% of the modules installed in the nation. CdTe has become the dominant source of modules in utility-scale projects, which make up 55% of total solar installs in the United States.

The US Department of Energy (DOE) recently launched the $20 million Cadmium Telluride Accelerator Consortium, which has a goal of making CdTe solar cells less expensive and more efficient, and to develop new markets for solar products.

First Solar is often touted as the lone US solar manufacturing success story, at least operating at gigawatt-scale. Founded in 1999, the company has had a manufacturing presence in Ohio since 2002 when it produced 1.5 MW of modules and employed 150 people. Since then, it has invested over $2 billion in expanding its Ohio manufacturing facilities.

In 2019 First Solar commissioned a second US factory, thus establishing itself as having one of the largest solar manufacturing footprints in the Western Hemisphere. Now a third factory is under construction. Representing an investment of $680 million, it will bring First Solar’s Ohio manufacturing capacity to 6 GW. The new “smart factory” will use artificial intelligence and Internet of Things connectivity, enabling the three-factory operation to have the capacity to produce on average one module roughly every 2.75 seconds.

Toledo Solar is another US manufacturer of CdTe modules. pv magazine USA spoke with founder, Aaron Bates, who noted several advantages to CdTe in the utility market beginning with that the degradation level is much lower than polysilicon modules. CdTe modules also perform better in high temperatures, and they’re highly recyclable. Bates credits First Solar for pioneering CdTe module recycling.

What’s in the Inflation Reduction Act of 2022 for US manufacturing?

- An investment of $30 billion in production tax credits to accelerate domestic manufacturing of solar panels, wind turbines, batteries, and critical minerals processing.

- A $10 billion investment tax credit to build clean technology manufacturing facilities, including those that make electric vehicles, wind turbines and solar panels

- $500 million in the Defense Production Act for heat pumps and critical minerals processing

- $2 billion in grants to retool existing auto manufacturing facilities to manufacture clean vehicles

- Up to $20 billion in loans to build new clean vehicle manufacturing facilities across the United States

- $2 billion for National Labs to accelerate breakthrough energy research

Tax credits across the solar supply chain

- Manufacturing credit: 100% credit through 2029, 75% in 2030, 50% in 2031, 25% in 2032

- Thin-film and crystalline silicon cells: $.04 per cell capacity in Wdc

- Photovoltaic wafers: $12/m²

- Solar-grade polysilicon: $3/kg

- Polymeric backsheets: $0.04/m²

- Solar modules: $0.07 per module capacity in Wdc

- Torque tubes: $0.87/kg

- Structural fasteners: $2.28/kg

- Central inverters: $0.25 per capacity Wac

- Commercial inverters: $0.015 per capacity Wac

- Residential inverters: $0.06 per capacity Wac

- Microinverters: $0.11 per capacity on Wac

- Battery modules: $10 per battery module capacity kWh

- Critical minerals: 10% of costs incurred

- Battery cells: $35 per battery cell capacity kWh

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.