From pv magazine 05/2021

Heterojunction (HJT) technology may be a well-established pathway to beyond 24% cell efficiencies, and there is some momentum among manufacturers to build up HJT production capacities. However, the high capex costs for HJT lines, some three times higher than that required for PERC, is understood by many to have been a break on the technology’s more widespread adoption – despite HJT’s numerous performance advantages.

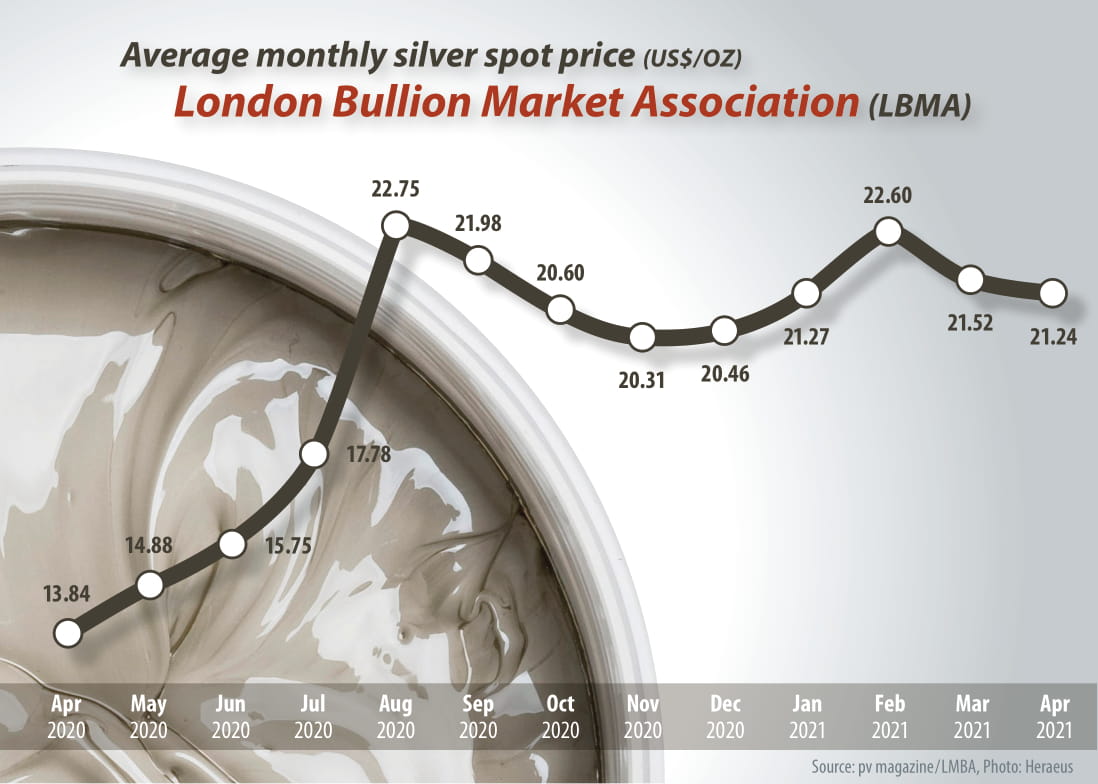

Beyond this investment hurdle, there are also concerns about HJT’s usage of technology-critical elements such as indium, used in the indium-tin-oxide (ITO) layer within a HJT cell, along with silver, a precious metal that has seen significant price increases over the past 12 months.

HJT cells require more than double the silver content, for cell metallization, than the mainstream p-type PERC. BloombergNEF reports that not only does HJT require more silver in its metallization pastes, the prices for the low temperature pastes for HJT come at a 20% price premium over pastes used for PERC.

“You cannot do a high temperature firing at 750-800 C like a normal PERC cell, you have to limit your temperature to around 200 C,” says Pierre Verlinden, the veteran solar researcher and former chief scientist at Trina Solar. Verlinden now heads the PV consultancy Amrock and explains that as lower temperature paste has a lower conductivity, it requires a higher silver content. “In addition, you have to put the same amount of silver on the back side, but for a PERC cell you put [far lower cost] aluminum on the backside instead,” he says.

Limit to scale

Given this, Verlinden raises serious doubts as to whether existing HJT technology can be a mainstream PV cell technology, if the solar industry is to scale to the multi-terawatt scale required for it to become a pillar of the zero-carbon economy of the future. “There is something around 10-20 GW of announced new capacity HJT in China. But the big issue I see is how will the existing HJT technology ramp up to 100 GW or terawatt level.”

Verlinden is not alone in this opinion. Taiwan-based PVInfoLink also notes silver costs as being a limited factor of both major n-type technologies – HJT and TOPCon, the latter requiring 50-75% more silver than PERC.

“Once cell manufacturers and vertically integrated companies ramp up gigawatt-scale n-type cell capacity expansions, the consumption of silver paste and cost control will become issues,” says PVInfoLink’s Corrine Lin. “As the global economy rebounds from the Covid-19 recession, demand for silver will rise significantly from PV and the many other industries where the material is used.”

Price increases

Even short term HJT plans, both by existing PV manufacturers and prospective new entrants, may be threatened or at least paused by the recent price developments in silver trading. Already some gigawatt HJT plans in China are not proceeding as previously announced.

The U.S.-based Silver Institute notes that the average annual silver price rose from $16.19 per ounce in 2019 to $20.52 last year – representing a 27% hike. The organization’s forecast for 2021 is “exceptionally encouraging” – unless you’re a HJT manufacturer – with prices expected to hit $30 per ounce, a seven-year high.

“Although silver loadings continue to drift lower,” wrote the Silver Institute, in its price forecast issued in February, “the sector will benefit from a growing number of countries that are installing new PV capacity.”

Reducing consumption

It is possible that silver paste laydown and the silver content within HJT pastes will come down, as HJT activities intensify and silver paste suppliers and manufacturers dedicate more R&D investment into paste development. After all, a similar process occurred with PERC pastes last decade.

German metallization equipment supplier Asys reports that, beyond silver consumption alone, it expects HJT printing times to improve as pastes become optimized. “There will be this development in the [HJT] pastes in near future so that the same print speeds with PERC cells can be achieved with the HJT pastes,” says Matthias Drews, the director of solar sales for Asys. “A lot of paste suppliers are working on this to make them [HJT pastes] easier to use and to reduce drying times.”

Perhaps most promising is the deployment of cell interconnection technologies such as multibusbars (MBBs) and “busbarless” concepts such as Smartwire, which Meyer Burger is deploying in its dual 400 MW production sites in Germany. The deployment of MBB has been demonstrated to reduce silver paste laydown on PERC lines, and it may reduce the silver requirement of HJT.

The roadmaps of some HJT developers certainly point in this direction. Meyer Burger has long promoted the combination of its Smartwire and HJT as being an ideal combination – likely in no small part to the savings on silver. And while Meyer Burger won’t be supplying its Smartwire to Chinese manufacturers such as Risen, Canadian Solar and Tongwei that are pursing HJT on large scale pilot lines, they appear likely to be developing similar “busbarless” concepts with China’s homegrown cell interconnection partners such as Autowell and Chinese Wuxi Lead.

However, for Verlinden, this introduces its own challenges, with bismuth widely used in “busbarless” cell interconnection. “Bismuth is used for the low temperature soldering for the Smartwire or low temperature MBB,” says Verlinden. “Neither indium nor bismuth is sustainable,” particularly at very large scales.

To become mainstream technology at the terawatt level and to have a role to play in the fight against global climate change, Verlinden argues, the HJT manufacturers must solve these three major challenges for HJT: bring the capex to the same level as PERC, reduce silver consumption to less than 5 mg/W, and replace ITO with a sustainable TCO material without impacting the efficiency.

In April, independent precious metals research consultancy Metals Focus presented its World Silver Survey 2021. It found that the PV sector currently accounts for around 20% of global industrial silver consumption, which in turn accounts for 50% of global demand for the metal. If the terawatt-scale manufacturing Verlinden envisages is to deploy HJT, those numbers may very well skyrocket.

| Risen HJT cell efficiency, silver content roadmap | |||||||

| Year | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2026 |

| Silver usage (mg/cell) 158 mm wafer | 400 | 180 | 160 | 140 | 80 | 80 | 50 |

| Cell efficiency | 23.2% | 23.5% | 23.8% | 24.5% | 25% | 25% | 30% |

| Source: Risen Energy | |||||||

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.