From pv magazine Global

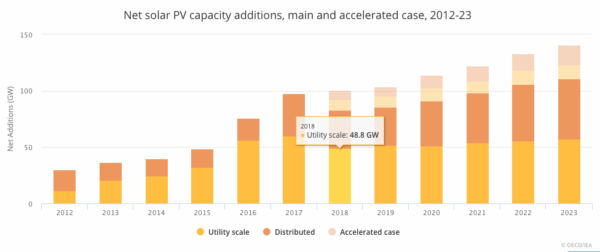

On Monday, the International Energy Agency released its latest forecast of global renewable energy markets, including numbers for solar PV deployment over the next five years. In the base case of Renewables 2018, the agency expects global solar PV deployment to fall 15% this year to 83 GW, but for installations to rise slowly thereafter to reach 111 GW in 2023.

IEA blames the short-term fall on Chinese policy changes. “The size of the global PV market over the forecast period is highly dependent on policies and market developments in China where the government decided to phase out feed-in tariffs (FITs) and introduced deployment quotas,” states IEA. “As a result, China’s solar PV deployment is expected to slow down, compared with 2017 growth levels. In the short term, global demand will decrease under the main case.”

The model also offers an “accelerated forecast” under which 101 GW of solar will be deployed this year, and for this to rise to 142 GW in 2023.

In terms of 2018 installations and the change from 2017 to 2018, IEA is notably more pessimistic than major market analysts. In forecasts released after China’s “5-31” policy change, IHS Markit estimated that the global solar market will still grow this year to reach 103 GW-DC, with Solar Power Europe forecasting 102 GW. IHS further expects 143 GW of solar installations globally in 2022 – faster growth than IEA even it its accelerated forecast.*

Both IEA and these other organizations agree that the reduction in Chinese support has led to lower module prices, which will spur demand globally. However, all major market analysts see this happening this year, and IEA is the lone holdout in stating that “demand recovery is expected after 2020”.

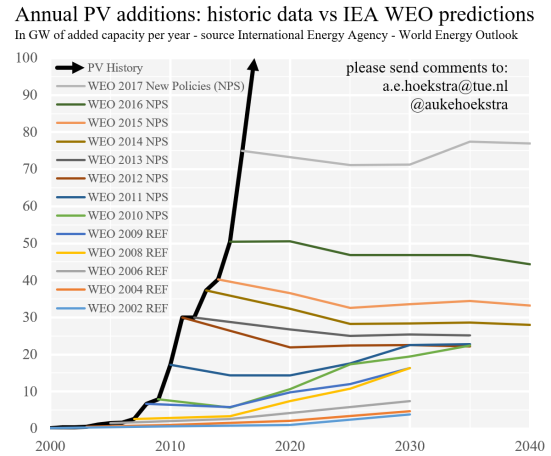

Unfortunately, such pessimistic forecasts are in line with a bad track record that the agency has of assuming relatively flat growth in solar deployment, versus the actual circumstances of exponential growth.

A year ago, TU Eindhoven Researcher Auke Hoekstra published a graph which demonstrates the divergence between solar market forecasts of IEA in its World Energy Outlook and the actual track record of solar markets.

A year ago, TU Eindhoven Researcher Auke Hoekstra published a graph which demonstrates the divergence between solar market forecasts of IEA in its World Energy Outlook and the actual track record of solar markets.

Even given its assumptions, IEA still expects 575 GW of solar to be deployed from 2018 through 2023, and for this to dominated renewable energy deployment. The agency also expects relative growth in distributed generation versus large-scale solar.

Update: This article was updated at 12:30 PM EST on October 9 to include the latest forecast by IHS Markit, which has reduced its 2018 estimate from 105 GW to 103 GW.

By Christian Roselund

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.