Bridge to India has released their latest edition of “India Solar Compass” – a quarterly update on the Indian solar market. As per the report, Q4 2017 was a slow quarter in terms of project commissioning, the sector witnessed only 1,503 MW of utility scale projects being commissioned.

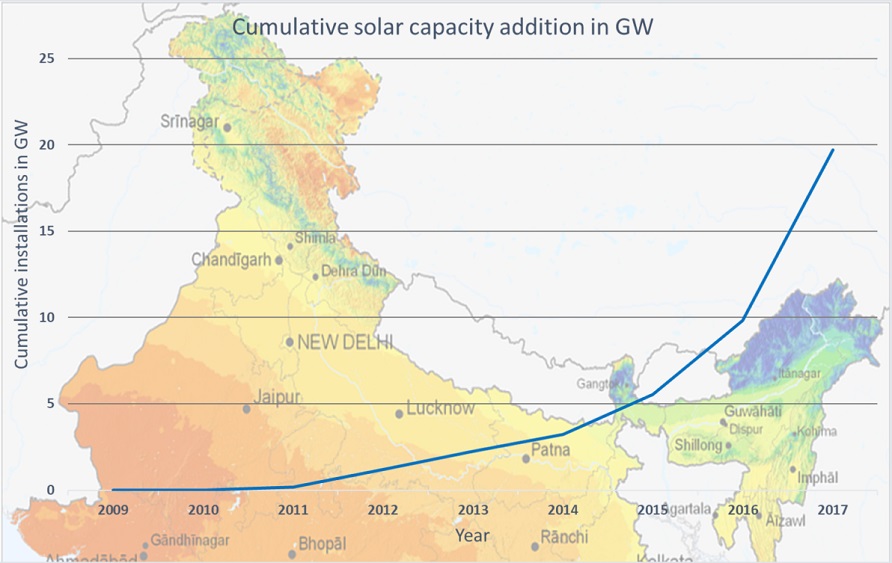

The report highlights that India’s total installed capacity reached 19,516 MW as of December 31, 2017. This includes utility scale solar capacity of 17,415 MW (89%) and rooftop solar capacity of 2,101 MW (11%). Yet again, the four southern states, along with Rajasthan, continued to lead the total installed capacity with a jump of up to 94% over 2016.

Speaking on launch of the report, Vinay Rustagi, Managing Director, Bridge to India, said, “The solar sector has been under pressure for some time due to a variety of factors – weak demand, increases in module prices, GST and threat of safeguard and/or anti-dumping duties. The impending decision on safeguard duty remains the overriding concern. But hopefully, the pick-up in tender issuance should provide some relief to developers and the overall supply chain.”

According to the report, Q4 2017 saw commissioning of only 1,503 MW of utility scale projects, as against a total of 5,100 MW scheduled/anticipated to be commissioned in the quarter.

The weak commissioning performance is mainly attributable to projects under various SECI, and Karnataka and Telangana state tenders. Developers cite procedural challenges in land acquisition and transmission connectivity, as well as module price increase (up 6% to $0.36/W in the quarter) as key reasons for the delays. The new safeguard duty investigation has also added to overall market anxiety.

Private sector

As in Q3 2017, ReNew commissioned the largest capacity in Q4 2017 (300 MW), followed by Adani (250) and Tata Power (180). ReNew also emerged as the largest developer by commissioned capacity (826 MW) for the whole of 2017, followed by Greenko (710) and NTPC (510).

In module supply, the top three suppliers—Canadian Solar, First Solar and JA Solar—had more than 50% market share for projects commissioned in Q4 2017. Amongst domestic module manufacturers, Mundra Solar (190 MW) and Vikram Solar (145) remained the largest manufacturers by production in the quarter.

In the inverter market, Sungrow captured a large market share (27%) in Q4 by supplying to projects commissioned in Telangana and Karnataka. It was followed by TMEIC – It is a joint venture between Toshiba and Mitsubishi Electric (20%), and Huawei (16%). The largest inverter supplier in the last two quarters, ABB, slid down to 7%.

Tender progress

As per the report, new tenders totaling 2,650 MW were issued in the quarter, up 50% over Q3 2017. Maharashtra (1,365 MW) and Karnataka (1,060) were the two main states to issue new tenders in the quarter. Rooftop solar also saw an encouraging growth of more than 100% in new tenders, aggregating to more than 220 MW.

Results were announced by SECI for its two Bhadla solar park based 500 MW and 250 MW tenders. Both tenders attracted high market interest with over-subscription of around 5 times. The winners include Hero (300 MW, INR 2.47/kWh), Softbank (200, 2.48), Azure (200, 2.48) and ReNew (50, 2.49). These tariffs are marginally higher than the previous low of INR 2.44/ kWh. But given that costs have continued to increase on account of GST, import duties, module price rises and other factors, they signal fierce competition amongst developers for winning new capacity.

Moreover, several projects and tenders has been cancelled amid WTO solar dispute between Indian and the United States.

Equipment and EPC cost trends

EPC costs has increased to INR 39/W (+5% over Q3 2017) in Q4 2017, mainly because of increase in module prices to $0.36/ W (+6%) and GST. According to the report, it is expected that the EPC costs to remain unchanged in Q1 2018 and reduce to INR 37/ W in Q2 2018. Moreover, the module prices to decline by $1-2 cents for each of the next two quarters. Meanwhile, prices of central inverters have been stable at INR 1.80/ W.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.