India’s EV sector secured INR 2.23 lakh crore in investments, just 18% of the capital needed by 2030: IEEFA

IEEFA states that bridging the INR 10.3 lakh crore investment gap over the next five years will require moving beyond traditional subsidy-led approaches toward structural risk-sharing mechanisms that lower the cost of credit and attract private capital in the electric mobility sector.

India’s electricity transition unfolds unevenly across states

A new report by IEEFA and Ember finds that India’s electricity transition is unfolding differently across states, shaped by variations in resource endowments, development pathways, and institutional capacities. While some states are already leading in renewable energy deployment and grid readiness, others are building momentum, presenting significant opportunities for accelerated progress through targeted, state-specific policy interventions.

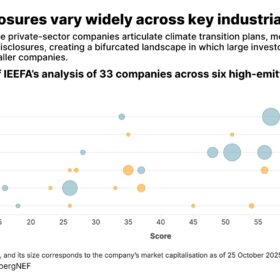

Credible transition plans key to unlocking decarbonization finance for India’s corporates

IEEFA’s assessment finds that while most companies have announced net-zero or emission reduction targets, only a limited number link these goals to capital expenditure plans, revenue assumptions or changes in business strategy, making it difficult for investors and lenders to assess the feasibility of transition pathways.

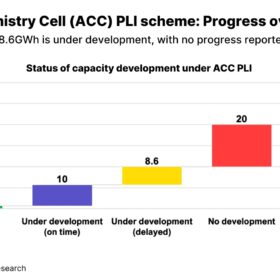

India’s PLI scheme achieves just 2.8% of targeted 50 GWh battery manufacturing capacity so far

Despite strong industry interest, India’s Advanced Chemistry Cell Production Linked Incentive (ACC PLI) scheme, launched in October 2021, is yet to translate policy ambition into realised capacity. As of October 2025, only 2.8% (1.4 GWh) of the targeted 50 GWh capacity has been commissioned within the stipulated timeline, entirely by Ola Electric—according to a new report by JMK Research and the Institute for Energy Economics and Financial Analysis (IEEFA).

Evaluating India’s corporate reporting framework for climate transition readiness: A BRSR–ISSB comparison

IEEFA’s analysis finds that the International Sustainability Standards Board (ISSB) S2 offers robust climate-specific guidance, while the Business Responsibility and Sustainability Reporting (BRSR) framework adopts a broader, ESG-oriented approach, with limited alignment to climate transition planning needs.

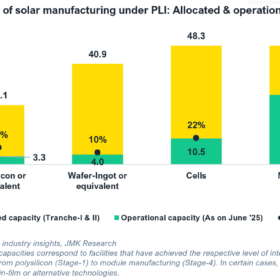

Solar PLI scheme drives strong industry interest but faces implementation challenges

As of June 2025, the overall achievement (operational capacity) rate of the solar PLI scheme stood at approximately 29% of the total awarded capacity. Capacity additions remain below targets, with only 59% of module capacity and 14% of polysilicon capacity achieved as of June 2025.

India must fast-track green hydrogen based steelmaking amid metallurgical coal supply risks: IEEFA

Indian steelmakers have begun adopting green hydrogen, but this option should become an even greater priority for the country as metallurgical coal supply risks intensify.

India needs targeted public finance to scale green steel: IEEFA

The country’s planned steel capacity expansion presents an opportunity to adopt cleaner technologies if supported by the right financing pathways.

India’s evolving battery landscape: An interview with Trina Solar’s Leo Zhao

Leo Zhao, Head of Energy Storage, Trina Solar Asia Pacific, speaks to pv magazine about why India is a strategic market for utility-scale energy storage, the latest trends and technology adoption, and Trina Solar’s plans for the market.

Jharkhand can emerge as a front-runner in India’s low-carbon transition

Jharkhand’s vast renewable energy potential, combined with its industrial base and critical mineral reserves, positions the state to emerge as a hub for low-carbon manufacturing, ranging from EVs, solar panels and battery energy storage systems (BESS) to green hydrogen production.