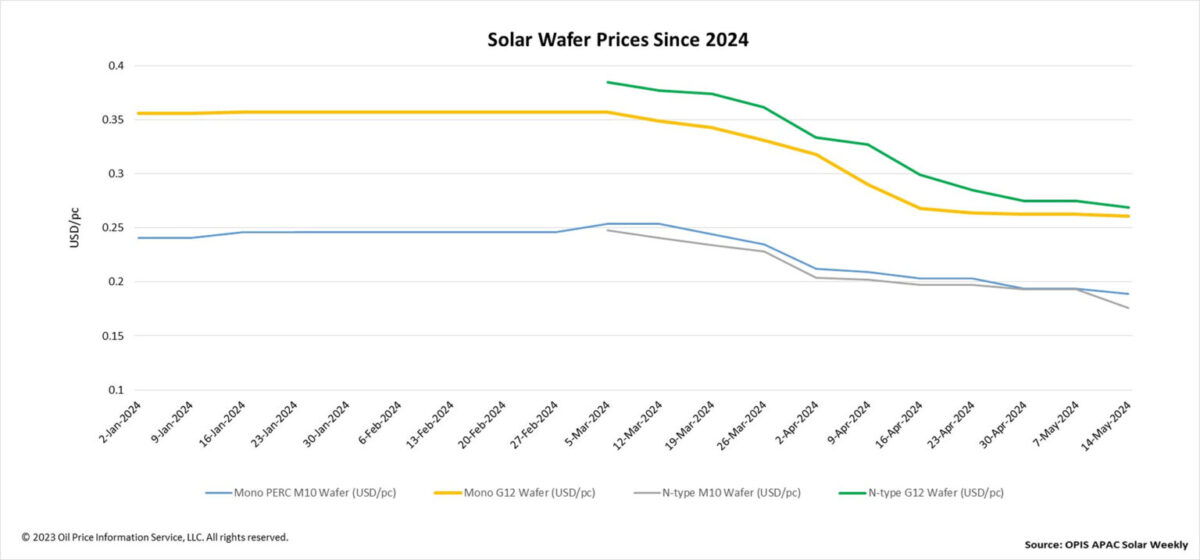

FOB China prices for wafers have experienced a widespread decline this week once again, underscoring the prevalent oversupply and the lackluster demand in the market. Mono PERC M10 and N-type M10 wafer prices decreased by 2.58% and 8.81% week-to-week, reaching $0.189 per pc and $0.176/pc, respectively.

Similarly, Mono PERC G12 and n-type G12 wafer prices dropped by 0.76% and 2.18% week-to-week at $0.261/pc and $0.269/pc, respectively.

According to OPIS’ market survey, the average transaction prices of Mono PERC M10 and N-type M10 wafers in the Chinese domestic market have descended to around CNY1.52 ($0.21)/pc and CNY1.41/pc, respectively. An industry insider even cited a transaction price of CNY1.35 for n-type M10 wafers, suggesting the potential direction of n-type wafer prices in the immediate future.

The wafer inventory remains high at approximately 4 billion pieces, equivalent to about 32 GW and half a month’s production, according to an upstream source. Amidst the backdrop of high wafer inventories, there have been reports this week of some manufacturers even increasing their operating rates.

“The majority of wafer producers who have ramped up their operating rates are specialized factories that have secured OEM orders,” a source explained.

Within the entire wafer market, crucibles and other single crystal growth furnace consumables such as graphite heat zone parts and carbon-carbon composites stand out as the only profitable segments currently, according to a market veteran. However, even the prices of these components have seen a significant decline, attributed to the diminished capacity of wafer manufacturers to bear the costs of auxiliary materials, the source said.

According to a market watcher, the business model of wafer manufacturers offers greater flexibility compared to the polysilicon producers. They can adjust their operating rates as needed, depending on their cash position, inventory status, and engagement in the OEM business model. However, as the source added, significant alterations to the supply and demand landscape may still require the inevitable closure and exit of certain wafer factories.

Several solar manufacturers have lately published their first-quarter 2024 financial reports, sparking considerable interest among industry insiders. According to a market watcher, this interest stems from the desire to uncover insights into the companies’ operational status and to gauge factors like the bottom price of products or the companies’ survival prospects.

Large wafer makers, despite incurring CNY billion cash losses due to extensive production capacity, can still maintain competitiveness since they hold a manufacturing cost advantage, the source further noted.

Another market participant elaborated that it’s challenging to predict when certain wafer manufacturers might go bankrupt to facilitate the improvement of the supply and demand pattern. Factors such as the cash flow status, financing capability, and whether a wafer company has a background in state-owned enterprises contribute to the uncertainty surrounding the survival timeline of each wafer company in the market.

In the global market, industry discussions have revolved around the potential for expanded domestic production capacity for modules and cells in the U.S., which could spur the nation’s demand for wafers from Southeast Asia. However, a market observer highlighted that significant demand for wafers in the U.S. may arise only after cell production projects are established, a process that typically spans 18 to 24 months.

Additionally, the source added that most of the wafer production capacity in Southeast Asia is currently owned by vertically integrated manufacturers who primarily utilize it for their own cell and module production within the region and seldom sell wafers externally. Consequently, the source anticipates the accelerated emergence of more wafer production capacity in Southeast Asia over the next two years, given the region’s status as a mature market for solar manufacturing.

Recent news releases on production capacity also seem to support this observation. According to OPIS data from the past two months, there have been no fewer than five updates on wafer projects in Southeast Asia. This week, it was announced that US-based SEG Solar signed a Land Utilization Agreement to establish its integrated PV manufacturing hub, including a 5 GW wafer factory, in Indonesia.

Additionally, Singapore-based G-Star announced on April 30 the commencement of construction at its 3 GW ingot/wafer plant in Indonesia. VSUN began production at its 4 GW wafer factory in Vietnam on April 18, while Astronergy started production at its 5 GW wafer factory in Thailand on April 15. Furthermore, Imperial Star announced on March 16 that the company is nearing the start of production at its 4 GW wafer plant in Laos.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.