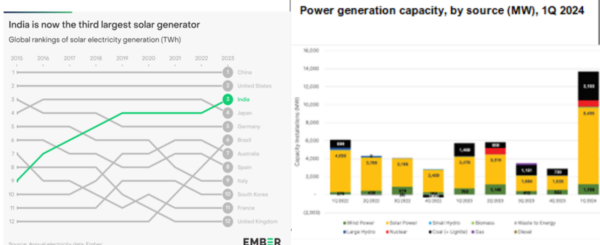

India added ‘record’ 13,669 MW of power generation capacity in the Jan-Mar period of this year (2024), with renewable energy contributing 71.5%. Coal’s share (including lignite) in the total power capacity dropped below 50% for the first time since the 1960s. This is well ahead of the Government of India’s target to establish 50% cumulative power generation capacity from non-fossil fuel-based sources by 2030, according to the latest POWERup quarterly report from the Institute for Energy Economics and Financial Analysis (IEEFA).

The report states that the decline in coal’s share mirrors a global trend, with the demand for coal in G7 countries plumbing record lows in 2023, levels not seen since 1900. To accelerate the transition, G7 countries last month vowed to phase out all unabated coal power generation by 2035, expanding on their commitment to end all construction of new coal-fired power plants.

As 2024 shapes as a pivotal year in the global transition away from fossil fuels, India is at the forefront, making great strides towards the target of Net Zero greenhouse gas emissions. Large-scale renewable energy projects have been the focus of intense interest, as evidenced by tender issuances crossing a record 69 GW, according to the report, ‘Utility-scale renewable energy tendering trends in India,’ released recently by IEEFA and JMK Research.

The tenders issued for utility-scale renewable energy projects in FY 2024 far surpassed the government’s seemingly ambitious target of 50 GW.

“After a slump from 2019 to 2022 due to supply-chain issues and global price spikes brought on by the Covid-19 pandemic and Russia’s invasion of Ukraine, the market has rebounded and gone from strength to strength,” says the report’s contributing author, Vibhuti Garg, director – South Asia, IEEFA.

“There is strong investor interest in the Indian utility-scale renewable energy market. The primary reasons are the large-scale potential for market growth, central government support in terms of targets and regulatory frameworks, and higher operating margins.”

India has rocketed to third in the world’s solar power generation rankings, behind only China and the US, according to Ember’s fifth annual Global Electricity Review of 80 countries, released last week. Ranked ninth in 2015, India has now surpassed Japan, which, along with fellow G7 member Germany, has a stubbornly high demand for coal.

Solar was the world’s fastest-growing electricity source for the 19th straight year, adding more than twice as much new electricity as coal last year. India had the world’s fourth-largest increase in solar generation in 2023 (+18 TWh), behind China (+156 TWh), the US (+33 TWh) and Brazil (+22 TWh). The top four countries accounted for three-quarters of solar growth in 2023.

Since 2000, the share of global electricity from renewables has expanded from 19% to more than 30%, driven by an increase in solar and wind from 0.2% in 2000 to a record 13.4% in 2023. As a result, the carbon dioxide intensity of global power generation reached a record low in 2023, 12% below the 2007 peak.

“A renewables-powered future is now becoming a reality,” said Aditya Lolla, Ember’s Asia programme director. “Solar power, in particular, is growing at an unprecedented pace. Our report concludes that the rapid growth in solar and wind has brought the world to a crucial turning point – likely this year – where fossil generation starts to decline at a global level.”

India generated 5.8% of its electricity from solar in 2023, in line with the global average, which hit an all-time of 5.5% in 2023. The nation, on the other hand, has been unable to shed its dependence on coal.

“Adverse weather conditions and surging power demand mean the country continues to rely on coal for over 70% of its electricity generation. The situation is unlikely to change this year, with the Central Electricity Authority expecting a shortfall in hydropower, leading to power shortages, especially during the night when solar is offline. As a result, the country may fire up idled coal plants to meet the shortfall,” states the report.

On a more positive note, India’s push towards renewable energy has attracted a host of new players at state, national and international level. Of the record 69 GW in tenders awarded in FY2024, only a quarter were from the Solar Energy Corp. of India (SECI), highlighting the important role that state-level authorities will play in the country’s utility-scale renewable energy landscape.

India has already installed ‘record’ solar power capacity of 8.5 GW during the first quarter of this year (2024), driven by many projects coming online, including Adani’s 1.6GW solar project at Khavda in Gujarat.

“The record solar installations were driven by a sustained year-on-year increase in tendered capacity and the urgency in commissioning of projects prior to the onset of the Approved List of Models and Manufacturers (ALMM) policy from April 1, 2024,” says Charith Konda, IEEFA’s energy specialist, India mobility and new energy.

The future looks bright for India’s renewable energy sector as innovative tender types emerge to meet the market’s needs. There has been an exponential rise of tender issuance for energy storage systems (ESS) projects, which will form a crucial part of India’s renewable energy infrastructure.

“Energy offtakers’ preference for a less intermittent and improved profile of renewable energy output has increased considerably,” says the report’s contributing author Jyoti Gulia, founder, JMK Research. “Since the introduction of hybrid tenders in 2018, renewable energy tendering has witnessed a strong shift in momentum from solar and wind to hybrid and renewable energy plus ESS. The emphasis on output power quality will continue to strengthen in coming years.”

Tendering activity in FY2024 reaffirms that the future for India’s renewable energy sector is bright, with market stakeholders confident the annual tendering capacity will again cross the national target of 50 GW in FY2025.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

5 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.