The Solar Energy Corporation of India (SECI) recently tendered projects to supply firm and predictable power to meet the peak requirements of DISCOMs, which otherwise have to depend on spot markets without price, supply or network assurance, and are prepaid. The tender was oversubscribed, with bids received for 1620 MW against the 1200 MW.

On a closer introspection these types of projects can be modelled to address the non-homogenous renewable energy proliferation in the country. This article proposes such a mechanism for annual balancing of firm power to address two key DISCOM issues, renewable purchase obligation (RPO) compliance and concern over high RE addition.

Base load vs peak load

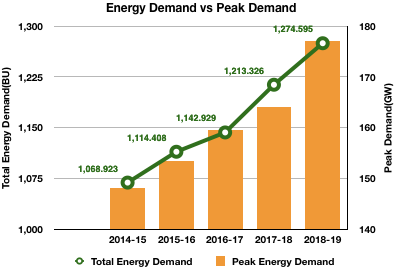

Over the last three years, India’s energy consumption has grown at a rate of 5.6% with a 6% increase in peak demand. This gradual increase in overall energy demand as well as peak demand has been accommodated with increase in variability of demand during the day as well as across seasons. However, the gap between maximum and minimum demand witnessed on grid has been increasing consistently, making it difficult to operate the grid with just base load power plants.

As per the Power System Operation Corporation (POSOCO)-National Load Dispatch Centre, in FY 18 alone, states witnessed more than 50% difference between peak load and base load. States like Telangana and Maharashtra are experiencing peak and base load difference of 100% and 40%, respectively.

Source: POSOCO

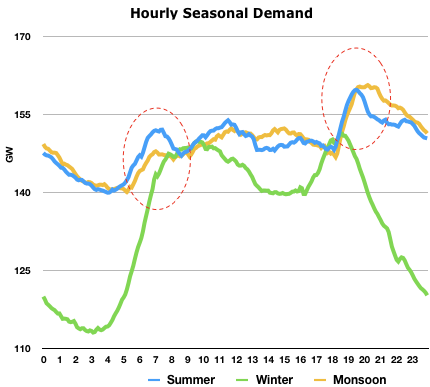

POSOCO data reveals that peak demand during summer increased by 20% from 130 GW (FY16) to 160 GW (FY 18) and base load demand in FY 18 during summer has increased by 17% to 140 GW. However, it is interesting to note that the difference between peak load and base load is 35%–a sharp 10% increase in two years during winter.

This increasing ramp rate requires flexible capacity with fast response time. Overall this trend from POSOCO indicates two interesting future trends: sustained increase in base load and peak load demand and widening of difference between peak and base load.

Image: POSOCO

Renewable Purchase Obligation

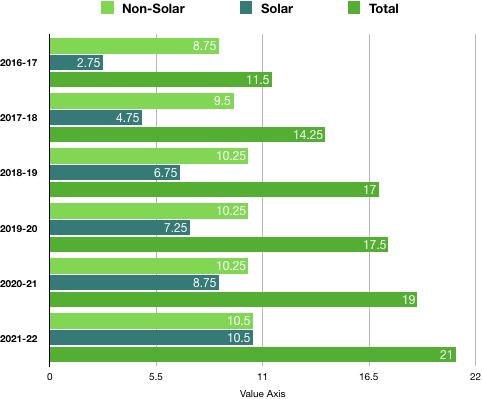

India’s National Tariff Policy was amended in January 2011 to prescribe solar-specific RPO be increased from a minimum of 0.25 per cent in 2012 to 3 per cent by 2022.

Central Electricity Regulatory Commission (CERC) and State Electricity Regulatory Commission (SERCs) have issued various regulations including solar RPOs, renewable energy certificate (REC) framework, tariff, grid connectivity and forecasting to promote solar energy. Consequently, in adherence to this, many states have come up with up their own solar policy.

After India’s renewable energy targets were revised, Ministry of Power in 2016 notified the long term growth trajectory of RPOs for non-solar as well as solar, uniformly for all States/Union Territories, initially for 3 years from 2016-17 to 2018-19. Further to this order, in June 2018 the ministry issued a directive for the next 3 years until 2022. According to this order, around 21% of total power consumed by each state should be derived from renewables (excluding hydro power generation) with half of it coming from solar power generation.

Source: Ministry of Power order 22.7.16 and 14.6.18

In the generation context, the last 5 years witnessed overall capacity increase by more than 50% propelled by capacity addition from solar and wind. However, this addition was only confined to a few states, resulting in a geographically skewed proliferation.

RE capacity development primarily has been confined to only 8-9 states, while REC based capacity development has been confined to only 6-7 states and finally competitive bidding has further skewed RE capacity development to only two-three states.

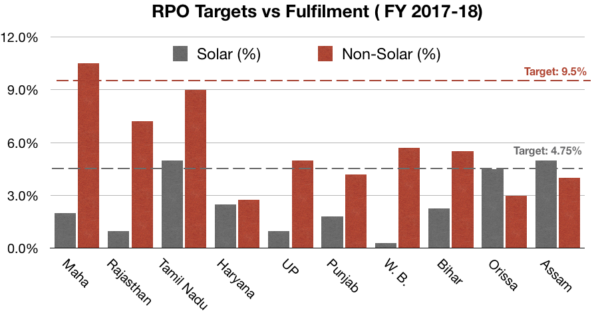

Most of the states in Northern, Eastern and Western regions have lower solar and non-solar RPO than Ministry of Power (MoP) specified National RPO trajectory (as seen in Fig. 4). Even with reduced level, many states in these regions have not been able to meet their RPOs. Besides difficulty in RE access, lenient enforcement, absence of penalties and RPO carry-forward are abetting RPO non-compliance.

NSEFI

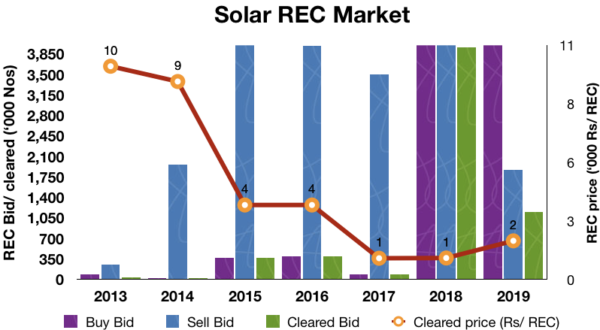

On the other hand, the quantum of REC market in the last 6-7 years highlights prevalence of buyer’s market while the price of solar (and non-solar) REC has decreased over these years. Despite adequate availability of solar and non-solar RECs in the market, state utilities have failed to comply with their RPOs, which suggests that DISCOMs are not preferring REC for RPO fulfilment.

NSEFI

Prevailing issues

RE development is taking place in limited pockets leveraging maximum resources, while areas with moderate RE potential are being neglected. States like Andhra Pradesh, Karnataka and Gujarat which were early RE leaders and which helped achieve the scale and cost reductions in today’s RE market, have already crossed RPO compliance trajectories. These states are now reluctant to develop further RE capacities despite having substantial untapped RE potential, land and evacuation infrastructure. On the other hand, procurement to comply with RPO is proving to be costlier for RE deficit states through short-term tenders.

Geographically limited RE development is also leading to inadequate evacuation infrastructure availability and since this infrastructure development has a longer gestation period, RE capacity development is delayed.

The solution – annual RE balancing mechanism

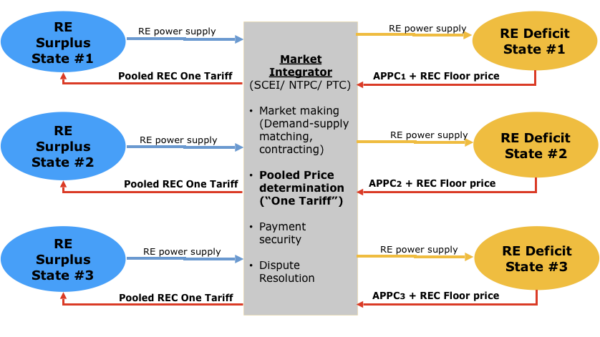

A simple annual RE balancing mechanism can help address two critical issues facing utilities today, RPO compliance and concern over RE addition. In this mechanism as illustrated in Fig. 6, an RE surplus state will supply firm schedule RE power (from any source like solar, wind or a combination thereof and/or with storage) from its RE generation pool on day-ahead schedule to deficit state.

The RE deficit state will have an assured availability of firm RE supply and can better manage its demand and grid based on such power. In return, the surplus state will receive ‘pooled’ RE tariff for the power supplied. In case, ‘pooled’ RE tariff is less than the respective surplus state’s weighted average RE cost, central government may support the surplus state.

The key factor here is the price discovery mechanism, which can be done through a market integrator (centralized body like SECI or NTPC). Market integrator can solicit demand from RE deficit states and also RE quantum available from surplus states during different months in a year and hours of the day. The integrator can then finalize cumulative RE demand-supply, supply period and determine a pooled RE tariff for buyers.

NSEFI

As mentioned, this pooled tariff can well be the sum of weighted average price of average power purchase cost (APPC) of the states from which the power is pooled and the REC floor price deducting the support received from the centre in terms of grant.

In this way, over the years, RE deficit states would be able to source firm, schedulable RE power at below APPC price. As the current average power purchase price (APPC) of most of the RE deficit states is in range of Rs 3.5 – 4/ unit, considering REC floor price of Rs 1.0/ unit, RE deficit states shall be able to procure firm RE power at Rs 4.5-5/unit for RPO compliance as well as demand management. In the coming years, APPC of RE deficit states shall increase while average RE supply cost of surplus states would reduce, enabling them to supply firm RE power below deficit state’s APPC price.

Benefits

With this pan India bundling, renewable energy can be sourced from the entire portfolio of surplus states rather than from any particular project/RE source while the tariff will be competitive compared to the escalating firm thermal power tariffs. While utilities in RE deficit states can use this to manage their short term demands and RPO on annual basis, RE surplus states can add new low-cost RE capacities bringing down their weighted average cost that can be passed on to deficit RE states. More than anything else, this mechanism will unlock the potential and help us in leveraging existing resources and infrastructure to achieve RPO and take us closer to the 175 GW target.

However, for this mechanism to become successful, the government of India should enforce the RPO strictly and uniformly across the country while addressing the issues related to Inter State Transmission System (ISTS). Waiving of Central Transmission Utilities (CTU) charges on annual RE transactions between States/Discoms for balancing RE power in-line with RE power bought directly from the generators on long term basis would be a crucial enabler. The central government may also consider incentivising states for adding all forms of RE capacity till 2022 for inter-state, intra-state, third party or captive consumption.

As NSEFI Chairman Pranav R Mehta says, “With the recent SECI tender, thermal power in India has become priced out. The most recent thermal power tenders in the country have resulted in levelised tariffs in the range of Rs 5.00-7.00/kWh @ 85% annual PLF (Cents 6.94-9.72/kWh). The peak tariff under this SECI tender is highly competitive vis-à-vis the recent peak tariffs in international markets like USA (Rs 8-9/kWh, or Cents 11.11-12.50/kWh).”

With the peak time-of-day tariffs becoming more and more pronounced in India, these discovered tariffs will be value accretive for DISCOMs, and are already much lower than the ever-increasing commercial & industrial consumer tariffs in India. Hence such annual RE balancing mechanism will go a long way in further inculcating RE into the grid.

India is at a crucial juncture of its RE journey. With the proposed mechanism (which can be refined through stakeholder engagement), the government can attempt to solve two of its longest prevailing problems, the DISCOM woes and RPO compliance with one shot.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

I “lost my comment” before I could complete it…. can it be restored… and sent to my email???

Hello sir,

I am so sorry, I can’t see your comment as saved…So if possible, pl do write again. Apologies for the inconvenience caused.

Best,

Uma Gupta

RE should just be integrated in the Grid…. just like other power sources …… Coal, Oil, Nuclear, Hydro, etc… which, except for Hydro, ALL consume Fuel and cause, short or long term, Pollution.

If there is Sunshine with or without clouds…. either you use it or lose it.

Let the Governors and Voltage Regulators Ramp Up/Down Generation from other sources… as has been done for a 100+years now on ALL UTILITY GRIDS…. nothing new here.

All this “hoopla” about RE Storage is… hoopla!! RE will have an impact on Grids only when RE becomes a major (60-70%) Generating Source… till then…. focus on RE …. specially Agrivoltaics.

Agrivoltaics may make POSCO’S redundant as Decentralized Generation … and Energy Independent Villages in Rural India come into being….. WITHOUT POLLUTION AND FULLY CLEAN RENEWABLE… TOO…

Yes…. one could also build small(er) Water/Energy Storage Resevoirs for Power Generation at night if necessary… for FULL GRID INDEPENDENCY…..why do we need POSCO’S or National Grids…. any more…. nothing to Balance, Transfer, Control etc…

Urban India can do the same too… if it wants… but (National and State) Urban Development Ministries and Bodies have a 100% Failure Track Record (see ALL our Urban Centers… The Big, Small and In Between) as in place of planned metros, cities and towns…. they spread misery for ALL. Can one rely on this method for the future….???