India’s energy transition is becoming an economic story

Large Indian corporations are no longer adopting renewable energy solely to strengthen ESG positioning. Increasingly, renewable procurement is being driven by commercial considerations: lower long-term electricity costs, reduced exposure to fossil fuel volatility, and improving competitiveness in global markets that are rapidly introducing carbon-linked trade frameworks.

Why grid modernisation must precede energy transition targets

The future of energy is not merely renewable – it is intelligent, flexible, and resilient. This requires investment not only in generation assets, but also in transmission corridors, reactive compensation systems, digital controls, automation, and dependable high-voltage equipment.

Meeting the challenges of long life time PV on buildings

As Europe’s first generations of integrated PV systems age, researchers and industry actors are only beginning to explore the long-term realities of maintenance, compatibility and repair.

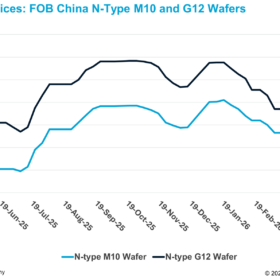

Chinese wafer producers build inventory ahead of expected Q3 demand recovery

In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

E-trucks: Unlocking the next frontier in India’s logistics transformation

As battery costs decline, charging networks mature, and financing models improve, e-trucks can move deeper into mainstream freight. India’s logistics transformation is no longer only about moving goods faster. It is about moving them with lower emissions, stronger energy security and better lifecycle economics.

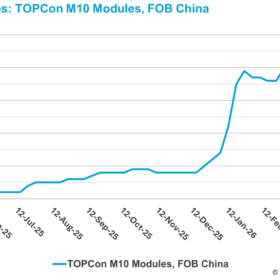

China TOPCon module prices hold steady as supplier price gap widens

In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

Solar approaches 3 TW, but the industry faces new challenges

Global solar PV capacity reached around 2,974 GW by end-2025, with nearly 698 GW added in 2025. The sector, however, is shifting from rapid deployment to integration challenges, as high penetration rates drive curtailment, storage demand, grid constraints, and evolving policy and market designs.

Can India’s steel pipe industry lead the global hydrogen infrastructure build-out?

One of the biggest constraints in the hydrogen economy today is the lack of transport infrastructure. Moving hydrogen remains expensive and logistically complex without pipelines.

Hybrid energy systems: Combining solar, wind & storage for maximum efficiency

Hybrid energy systems are set to play a crucial role in shaping the future of energy infrastructure. With advancements in smart grid technologies, artificial intelligence, and predictive analytics, these systems will become even more efficient and adaptive. They offer a scalable and sustainable solution to meet rising energy demands while reducing carbon emissions and enhancing energy security.

How distributed energy resources can help India meet its 2030 clean energy targets faster

Distributed energy resources, rooftop solar, C&I open-access systems, behind-the-meter storage, solar agricultural pumps, microgrids, share one decisive advantage: deployment speed. And speed is not the only advantage. Power consumed where it is generated avoids the 15-22% aggregate technical and commercial losses in India’s distribution networks.