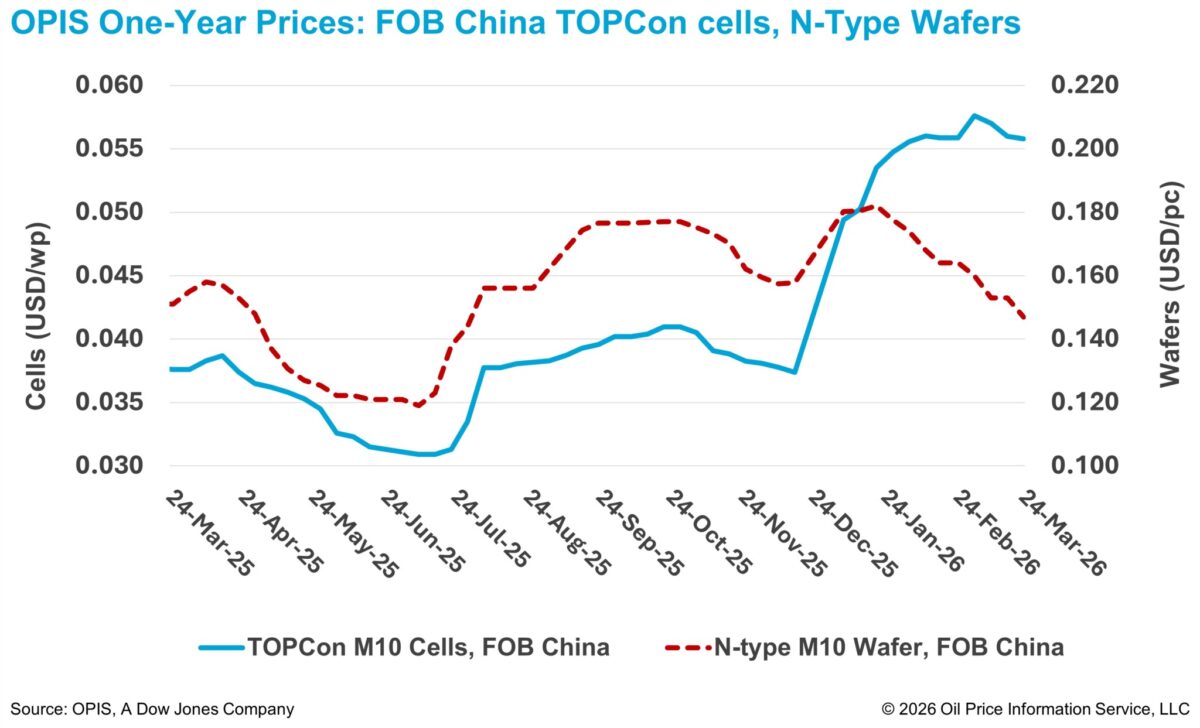

China’s TOPCon M10 solar cell prices fell for a third consecutive week, tracking declines in upstream polysilicon and wafer prices as production costs continued to ease. Demand remained bearish, with market participants still assessing the price outlook ahead of the April 1 cancellation of China’s export tax rebate on solar products.

According to the OPIS Global Solar Markets Report released on March 24, Free-On-Board (FOB) China TOPCon M10 cell prices fell 0.36% on the week to $0.0558/W with weaker price indications between $0.0535-0.0581/W. Meanwhile, FOB China prices for n-type M10 wafers declined 3.92% to $0.147/piece over the same period.

China’s solar cell production for January-February totaled around 98.3 GW, down 7.8% year-on-year, according to the National Bureau of Statistics. Market analysts said major cell manufacturers were only operating at around 40% capacity in January, leaving more than half of installed capacity idle. Producers were said to be proactively cutting output to reduce inventories and stabilize prices.

In addition, the surge in silver paste prices in January squeezed margins and discouraged further production, which may have also weighed on overall output, industry participants said. That cost pressure has since eased, however, with silver prices declining over 20% from their January peak.

Upstream wafer producers and traders continued to cut prices to reduce inventories and recover cash, placing further pressure on wafer prices, said the China Nonferrous Metals Industry Association (CNMIA).

On the demand side, end-market installation demand remained weak while continued pressure on cell prices weighed on overall wafer demand, CNMIA said. Wafer manufacturers have maintained normal production and currently have no plans to reduce operating rates, leaving supply relatively loose, the industry body added.

Cell exports, meanwhile, increased year-on-year. One market analyst said China’s cell exports totaled around 14 GW in January and February, compared with around 12.8 GW over the same period in 2025, according to data from global think tank Ember.

While cell prices continued to soften, module prices were relatively more supported, partly due to firmer costs for bill-of-materials inputs, according to market sources. A module manufacturer said higher natural gas prices have made solar glass production more expensive, while higher oil prices are driving up costs for ethylene vinyl acetate (EVA) and polyolefin elastomer (POE) encapsulation films used in module assembly.

Still, one market source told OPIS they expect module prices to continue to track cell price movements, given that cell prices make up a significant share of total module production costs.

Module purchasing activity in Q1 2026 has largely stalled amid price volatility following a rush to secure orders before the export tax rebate removal, according to buyer sources.

Market participants said some buyers believe the February-March price spike is likely to be temporary and could ease in Q2 2026 once front-loaded demand fades.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.