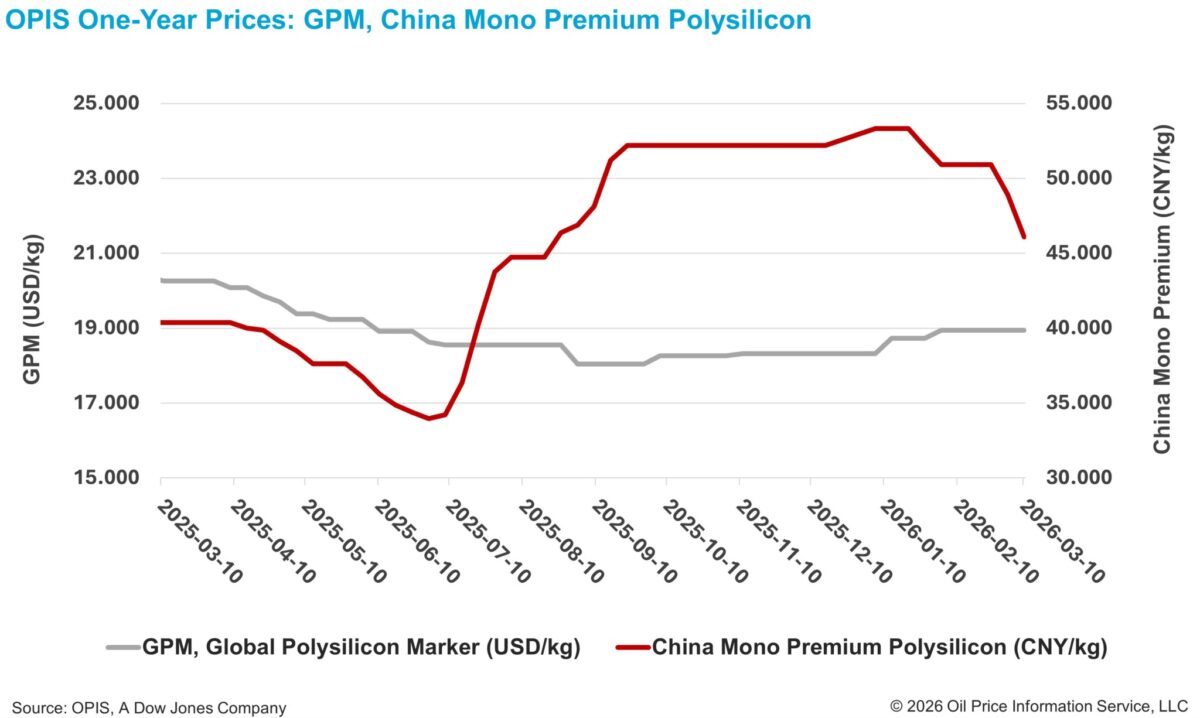

The China Mono Premium—OPIS’ assessment for mono-grade polysilicon used in n-type ingot production—was down 5.79% week on week at CNY 46.083 ($6.71)/kg, or CNY 0.097/W, according to the OPIS Global Solar Markets Report released on March 10.

Since the beginning of the year, the China Mono Premium has declined by more than 13%.

According to industry insiders, the polysilicon market is negotiating orders for late-March delivery, with some buyers reportedly only willing to place orders around a psychological price level of CNY 40/kg. A trade participant said a polysilicon price of CNY 40/kg would still not allow wafer manufacturers to avoid or minimize cash losses, adding that this level does not necessarily represent the price floor.

Another participant noted that although some leading manufacturers continue to quote around CNY 50/kg to slow the pace of declines, transaction prices from second- and third-tier producers have rarely exceeded CNY 45/kg since the end of the Lunar New Year holiday.

A major Chinese polysilicon producer announced last week that its total output reached approximately 123,700 metric ton (MT) in 2025, with a projected increase to 140,000–170,000 MT in 2026. The company disclosed that its polysilicon cash cost in Q4 2025 had declined to CNY 33.95/kg, while full cost stood at about CNY 43.46/kg. An industry insider noted that, given the company’s relatively limited inventory, its plan to moderately increase production in 2026 could help reduce overall costs—a strategy aimed at minimizing losses through more rational production management.

Nevertheless, inventories across the broader market remain substantial. Industry insiders widely acknowledge that stockpiles exceeding 500,000 MT could persist, with inventories potentially not normalizing until 2028-2030.

A market source said that as producers’ cash flow becomes increasingly tied up in inventory, major manufacturers may be compelled to sell at or near cash cost, at prices that do not fully cover depreciation, labor, working capital or taxes. The source added that under such conditions, the China Photovoltaic Industry Association’s (CPIA) recommendation that selling prices not fall below full cost would be difficult to achieve.

Although no official announcement has been made, industry reports indicate the CPIA recently issued a document estimating the average total cost of polysilicon in January 2026 at approximately CNY 54.125/kg. The association noted that some companies were selling at CNY 43–45/kg—17%–20% below that benchmark—and characterized such pricing as unfair competition falling outside the industry’s reasonable range.

Meanwhile, the global polysilicon market has shown signs of stabilization in recent weeks, with fewer updates on new trading activity compared with previous months.

According to the OPIS report, the Global Polysilicon Marker (GPM)—the OPIS benchmark for polysilicon produced outside China—was assessed at $18.942/kg, or $0.040/W, remaining unchanged from the previous week.

Market participants attributed the recent stabilization partly to the U.S. preliminary ruling on countervailing duties (CVD) targeting solar cells and modules imported from India, Indonesia and Laos. One participant noted that while barriers for solar products from these regions entering the U.S. have increased, downstream manufacturing capacity expansion in emerging markets remains limited, potentially weakening global demand for polysilicon.

The delayed release of findings from the U.S. Section 232 investigation into the national security implications of polysilicon and its derivatives has also added to uncertainty in the global polysilicon market. Despite earlier indications from insiders that the decision would not be delayed beyond March, recent reports suggest the announcement may now be postponed until after April 2026.

Industry insiders added that while the Section 232 outcome is unlikely to directly affect polysilicon prices in China, the overall stringency of the policy will likely reflect broader U.S.-China relations. A market participant noted that if relatively moderate restrictions on polysilicon and its derivatives are imposed, it could benefit non-U.S. polysilicon producers by creating a more accommodating downstream market environment, potentially supporting demand.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.