Bernreuter Research said in a new report that nine of the world’s 10 largest polysilicon manufacturers are based in China, with Tongwei, GCL Technology, Daqo New Energy and Xinte Energy holding a combined 65% share of global output in 2024.

All but one of the world’s top 10 polysilicon manufacturers are based in China, according to findings from Bernreuter Research.

Johannes Bernreuter, head of the German research company and polysilicon market expert, has published a ranking of the 10 leading polysilicon manufacturers globally, ordered according to actual output in 2024.

Since 2022, the top four positions in the ranking have been occupied by China’s Tongwei, GCL Technology, Daqo New Energy and Xinte Energy. Together, they accounted for a combined 65% of the market share last year, as well as two thirds of new polysilicon capacity developed since the start of the decade.

Tongwei has increased its total capacity almost tenfold since 2020, currently standing at approximately 910,000 metric tons across three factories, far exceeding second-place GCL Technology, which has a total capacity of 480,000 metric tons across four factories.

Daqo New Energy’s production capacity stands at around 350,000 metric tons, while Xinte Energy’s totals approximately 300,000 metric tons. “Therefore, it is no wonder that the top four also accumulated two thirds of the huge inventories at Chinese polysilicon manufacturers by the end of 2024,” Bernreuter said.

China’s Qinghai Lihao Qingneng, Xinjiang East Hope New Energy and Asia Silicon occupy positions five, six and seven in Bernreuter’s ranking.

The only non-Chinese company among the top ten is German-based chemicals group Wacker. Formerly the world’s largest polysilicon manufacturer from 2016 through 2019, the company sits in eighth this year with a production capacity of approximately 80,000 metric tons. Bernreuter’s analysis adds that the company remains the largest producer of semiconductor-grade polysilicon.

With a planned consolidation of China’s polysilicon industry in the works, Bernreuter expects Wacker to retain its position in the top ten through at least 2027. However, he added the prediction assumes the US solar market, which remains the leading destination of solar modules made from non-Chinese polysilicon, “recovers from the crackdown of the Trump administration on renewables”.

China’s Hongyuan Energy Technology Co. and Xinjiang Goens Energy Technology Co. round out the top ten, with production capacities of 60,000 and 65,000 metric tons. The former is a new entrant into the ranking and is viewed as a “mini version of market leader Tongwei” by Bernreuter due to its complete integration from polysilicon production through to solar module assembly.

Michigan-based Hemlock Semiconductor Operations was once a mainstay in the top 10, holding the polysilicon market leader position from 1994 to 2011. It dropped out of the top 10 in 2023 when the threshold for entry rose to 60,000 metric tons and stands in 14th position this year with a production capacity of approximately 35,000 metric tons (MT).

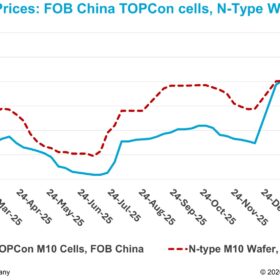

Analysis by Bernreuter Research published in June warned that the Chinese polysilicon industry risks triggering a global shortage by 2028 if manufacturers cut too much production capacity. At the time, Bernreuter reported China expanded polysilicon capacity to 3.25 million MT by the end of 2024, accounting for about 93.5% of global output and collapsing prices to below $4.50/kg.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.