India added 20.1 GW of renewable energy (RE) capacity in the first five months of FY2026 (April–August 2025), marking a robust 123% growth compared to 9 GW during the same period last year, according to a recent report by ICRA. This includes 17.5 GW of solar and 2.6 GW of wind capacity additions.

ICRA highlighted that this record growth—driven by a strong project pipeline and favorable market conditions—positions the sector to exceed 35 GW of new capacity in FY2026.

The growth momentum follows a strong performance in FY2025, when RE capacity addition rose to 28.7 GW from 18.5 GW in FY2024. ICRA stated that the current expansion is supported by a substantial project pipeline of 142.8 GW, as per the Central Electricity Authority, along with attractive solar module prices and robust electricity demand.

Despite the strong pipeline, the report notes a significant slowdown in bidding activity, with only 3.4 GW auctioned in the first half of FY2026. This is attributed to delays in the signing of Power Sale Agreements (PSAs) by bidding agencies with state distribution utilities, which, in turn, stalls the finalization of Power Purchase Agreements (PPAs) with winning developers. The timely execution of these agreements, along with the augmentation of transmission infrastructure, is identified as critical to sustaining the current growth trajectory.

ICRA maintains a Stable outlook for the RE sector, underpinned by strong policy support, the superior tariff competitiveness of renewables, and increasing sustainability commitments from large commercial and industrial (C&I) customers.

Key sector developments

Cost competitiveness boost: ICRA expects the recent reduction of Goods and Services Tax (GST) rates for solar PV modules and wind turbine generators—from 12% to 5%—to lower the capital cost for solar and wind power projects by about 5%. This is projected to reduce the cost of generation by 10 paise per unit for solar power and by 15-17 paise per unit for wind power.

Strong C&I demand: The demand outlook in the C&I segment, which comprises 45-50% of India’s electricity demand, remains highly favourable. Achieving a 20% RE penetration in this segment over the next five years would necessitate approximately 100 GW of RE capacity, implying a Compound Annual Growth Rate (CAGR) of almost 30%.

Energy storage gains traction: The quoted bid tariffs for BESS have seen a significant decline, improving the cost economics for hybrid projects. ICRA expects the energy storage capacity requirement to reach 50 GW by 2030, to be met through a mix of BESS and pumped storage hydro projects.

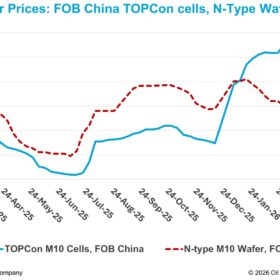

Module price dynamics: While prices for imported n-type modules remained low at about 8-9 cents/watt in August 2025, domestic prices were higher at 15-17 cents/watt due to the imposition of the Approved List of Modules and Manufacturers (ALMM). The upcoming imposition of ALMM on solar cells from June 2026 is likely to drive up module prices in FY2027 — a factor that developers must account for in future bids. The report also notes that the recent imposition of 50% tariffs by the US on India is expected to adversely affect the competitiveness and export volumes of Indian original equipment manufacturers.

Sector resilience: The credit profile of the RE sector remains resilient. In 5M FY2026, the sector recorded 15 upgrades against 13 downgrades, with upgrades driven by successful project commissioning, satisfactory generation performance, and favourable changes in ownership.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

2 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.