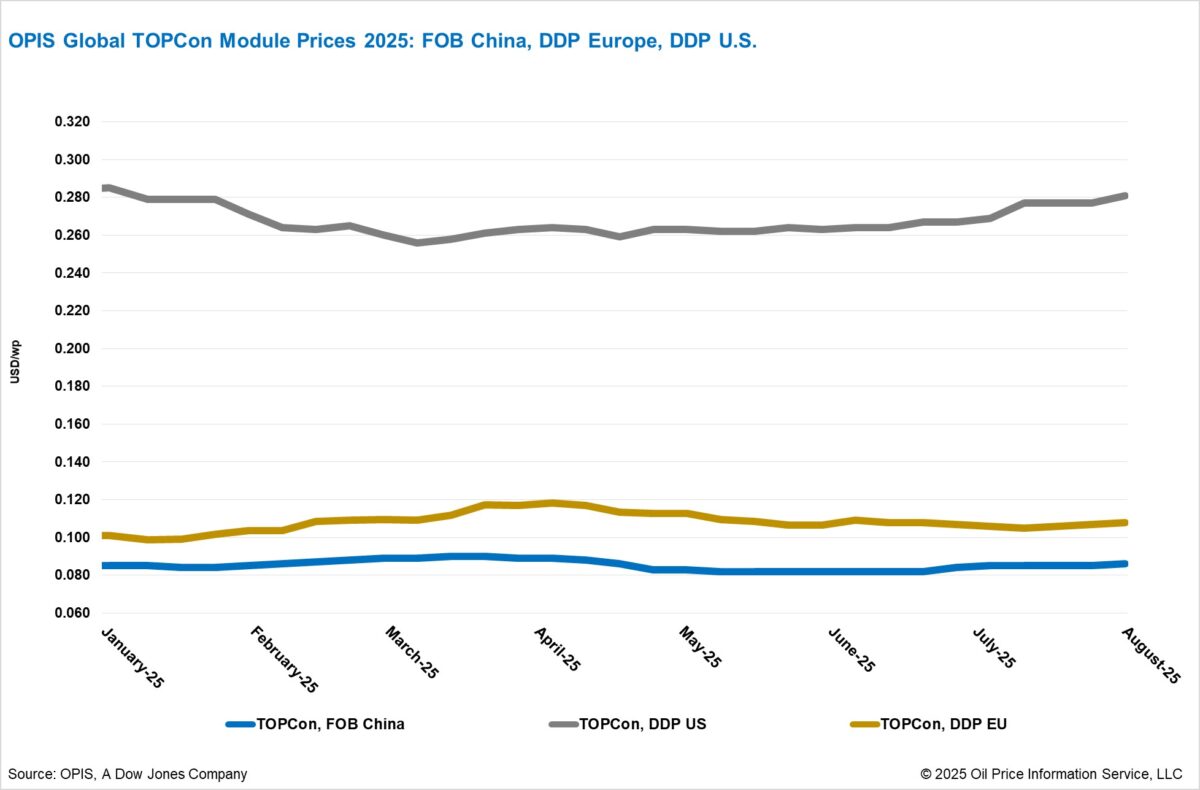

The Chinese Module Marker (CMM), OPIS’s benchmark for TOPCon modules ≥600W, rose 1.18% this week to $0.086/W Free-On-Board (FOB) China, with market indications between $0.084–0.093/W. Since the beginning of the second half of 2025, prices have recorded an increase of 4.88%.

Forward curve indications tracked the spot market higher. Prices for Q4 2025 loadings increased to $0.086/W, while Q1 and Q2 2026 remained steady at $0.086/W. Q3 2026 loadings edged higher to $0.087/W.

In the domestic market, OPIS assessed TOPCon prices at CNY 0.690 ($0.096)/W EXW China, up 0.73% week-on-week. Sentiment improved following a Ministry of Industry and Information Technology (MIIT)–led meeting, the second in H2 2025 aimed at curbing disorderly competition. Compared to the July session, the August meeting was broader, addressing four key areas: stronger regulation, restrictions on below-cost competition, stricter quality enforcement, and enhanced industry self-discipline.

Market speculation has centered on regulators potentially setting a minimum domestic sale price of CNY 0.75/W ($0.096/W FOB China with VAT). If implemented, this would mark a departure from the non-binding cost guidance issued by the China Photovoltaic Industry Association (CPIA), introducing enforceable legal measures. However, many participants remain cautious, questioning the sustainability of such levels given current inventory conditions.

CPIA has also called on local governments to enforce the Price Law, establish minimum bidding prices, and reduce the weight of price factors in tenders. The association emphasized rational production aligned to supply-demand dynamics, as well as quality assurance and intellectual property protection.

Recent tenders suggest improving sentiment. Huadian Group awarded a 20 GW module procurement for 2025–2026, with TOPCon bids averaging CNY 0.710/W, while China Resources Power’s 3 GW tender posted averages above CNY 0.70/W. These outcomes indicate market stabilization around higher price ranges.

In Europe, TOPCon module prices remained steady through the holiday season, with OPIS assessing DDP Europe prices at €0.092 ($0.11)/W for modules ≥600W.

However, higher-efficiency HJT products are drawing growing interest despite their price premium, with reported prices at €0.095/W for ≥600W modules and €0.105/W for ≤450W modules.

Domestic HJT manufacturing momentum is building. Italy-based Enel’s 3Sun already operate facilities, while Spain’s MCPV plans a 2.5 GW HJT plant. Bee Solar and China’s Huasun Energy signed a Letter of Intent to develop integrated HJT manufacturing in Italy, with operations targeted for 2026.

At the policy level, some governments are tightening support. France has cut tender volumes, while Sweden intends to reduce tax credits, creating headwinds. Nonetheless, new financing and projects continue: German developer Energiekontor launched a €15 million bond to fund solar and wind projects across Europe, while utility RWE secured 37 MW in new solar projects through a federal tender.

In the U.S., TOPCon ≥600W modules DDP US rose 1.44% to $0.277/W this week. Southeast Asia cargoes increased 1.14% to $0.267/W following reciprocal tariffs, while Indian cargoes fell 1.86% to $0.317/W amid weak demand linked to anti-dumping and countervailing duty (AD/CVD) probes.

Forward deals for suggest Q1 2026 prices at $0.276/W. U.S.-assembled modules using imported cells are generally quoted at $0.30–0.40/W, while those with domestic-content cells fetch $0.40–0.50/W, with occasional quotes above $0.60/W.

Uncertainty continues around trade and tax policy. The U.S. Treasury’s updated safe harbor rules removed the 5% spend option but were not applied retroactively, calming market concerns. Developers are rushing to secure safe-harbor deals before the September deadline, keeping short-term demand firm.

Meanwhile, inventories at U.S. assemblers are reportedly shrinking, with one large supplier holding only ~100 MW. The looming 2026 restrictions on Foreign Entity of Concern (FEOC) suppliers are expected to create pricing bifurcation between compliant and non-compliant modules. For now, opportunistic price increases linked to new tariffs are being observed, while Chinese producers explore shifting cell production to Africa to bypass restrictions.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.