Cell and module technologies are advancing faster than the market expected, said experts set to participate in the NetZero Milan Expo-Summit 2025, organized by FieraMilano and scheduled to take place from May 14 to May 16 in Milan, Italy.

The scheduled speakers have told pv magazine that the PV module landscape has rapidly evolved, driven by the mainstream adoption of n-type technologies.

“TOPCon has emerged as the leading successor to p-type PERC, offering higher efficiency and improved low-light performance. Mass-produced TOPCon modules now reach efficiencies of up to 23.8%. Heterojunction (HJT), once considered the next major step, is evolving more slowly than expected, with several manufacturers shifting their focus directly to back-contact (BC) technology,” said Yana Hryshko, head of solar supply chain research at Wood Mackenzie.

FuturaSun CEO Alessandro Barin said TOPCon cost reductions have been a definite game-changer.

“What was once a premium option is now increasingly competitive in terms of efficiency and manufacturing cost,” he said. “This is driving broader industry adoption and pushing module performance benchmarks higher across the board.”

Joris Libal, project manager at ISC Konstanz, said the recent introduction of laser-enhanced contact optimization (LECO) technology to the TOPCon manufacturing process will further accelerate this shift by delivering additional gains in cell and module efficiency.

“LECO, in addition to enabling higher efficiencies, will significantly reduce long-term reliability issues observed in certain types of TOPCon modules,” he said. “Advanced TOPCon technologies, such as selective passivated contacts on the rear side, will increase the bifacial factor of TOPCon modules to above 90%, thereby approaching the bifacial factor of heterojunction (HJT) modules.”

Francesco Emmolo, general manager for Italy and Greece at Longi, said the company is betting on combining HJT with back-contact designs and is emerging as the back-contact champion, with around 17 GW of back-contact products shipped in 2024.

“The most important innovation of the last 2 years from our point of view is our introduction of HPBC-based PV modules,” he said. “This is the first time that a Back contact-based cell design has been integrated into a mass-produced module, opening the availability of the most advanced cutting-edge technology to the mainstream market.”

“BC modules are already achieving impressive efficiencies above 24%, and while traditionally associated with premium residential and C&I segments, they are now increasingly deployed at utility scale, particularly in China,” said Hryshko, noting that perovskite tech is also advancing rapidly, with the first commercially available modules expected by 2026. “Although BC still has limited manufacturing capacity compared to TOPCon or HJT, its superior performance characteristics make it an attractive option across market segments.”

Rise of back contact

Libal said large-scale mass production and R&D efforts in China and Europe are driving down manufacturing costs of TOPCon back-contact cells and modules, rapidly narrowing the gap with standard TOPCon.

“TOPCon BC is gaining market share faster than forecasted by various roadmaps,” said Libal. “Accordingly, there is a strong likelihood that, by 2030 at the latest, TOPCon technology will replace pure TOPCon as the mainstream PV technology.”

The scientist said TOPCon and TOPCon BC are well-suited as bottom cells for future silicon-perovskite tandem modules, but noted that resolving reliability issues with perovskite layers will take time.

“Such tandem modules will not have any significant market share before 2030, or even later,” said Libal.

FuturaSun’s Barin noted the remarkable acceleration in the development of perovskite solar cells and their even greater future potential.

“Their high-efficiency potential, tunable bandgap, and compatibility with tandem configurations make them one of the most promising candidates for next-generation photovoltaics,” he said. “Research has rapidly advanced toward improving their stability and scalability, bringing commercial viability closer than ever”.

Hryshko said that another major development is the shift in module formats.

“The widespread adoption of larger wafer sizes (M10 and G12) and higher power classes, often exceeding 600W, has contributed to lowering balance-of-system (BOS) costs,” said Hryshko. “Bifacial modules have also become the norm in utility-scale projects due to their higher energy yield and diminishing price premium over monofacial designs.”

New scenarios

Hryshko said new encapsulant materials and advanced interconnection methods have improved module durability, helping products meet tougher climate and stress tests and boosting long-term reliability across more environments.

Experts disagreed on the impact of U.S. tariffs on Chinese cells and wafers. Hryshko said recent US-China tensions have had limited new effects on the solar sector, despite widespread assumptions.

“The US market has operated under restrictive trade policies – including AD/CVD tariffs, Section 201, and the Uyghur Forced Labor Prevention Act – for years. As a result, Chinese solar modules are already largely excluded from direct access to the US market,” she said. “While the US has developed a self-sufficient domestic module assembly capacity, it still relies heavily on imports for solar cells and wafers, which poses a risk to the full domestic supply chain build-out. However, with coordinated policy and investment, this bottleneck is addressable.”

It is clear that the new US political approach will require new commercial strategies.

“We already adapted somehow,” said Emmolo. “Currently, we have factories in Vietnam, Malaysia and the United States that help us to be more flexible in the supply chain.”

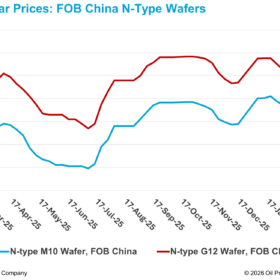

Hryshko said that the pricing distinction between high- and low-technology modules is narrowing.

“Current module prices have fallen below many manufacturers’ cost of production, and the price delta between TOPCon and BC technologies is minimal – generally around €0.005 ($v)/W to €0.01/W. Because the majority of global module supply comes from China, and Chinese manufacturers are largely absent from the US market, pricing is now more influenced by internal Chinese dynamics – such as overcapacity and domestic demand – than by external geopolitical tensions.”

The Global Solar Council has said that prices might stabilize this year and in 2026.

“Profit margins for manufacturers are likely to improve in H2 2026,” said Sonia Dunlop, the CEO of the Global Solar Council.

Europe is more vulnerable than the United States, said Hryshko, as it remains highly dependent on Chinese imports, with approximately 98% of its solar modules sourced from China.

“Unlike the US, Europe has minimal operational module manufacturing capacity and no effective trade barriers in place. While there is growing awareness of the risks, geopolitical and logistical, posed by this dependence, no decisive shift has occurred,” said Hryshko. “Given that solar is expected to account for 30% of the EU’s electricity generation by 2030, building a more diversified and resilient solar supply chain is a matter of both energy and national security. In this context, geopolitics must be weighed alongside industrial strategy.”

However, this situation will also create opportunities, especially for companies that can facilitate cross-border relationships through joint ventures.

“The current geopolitical landscape, while challenging for many, actually presents unique advantages for a company like ours. Our dual identity, being both Italian and Chinese, allows us to remain agile and resilient in the face of shifting trade dynamics and regulatory environments,” said Barin. “This positioning gives us greater flexibility in our supply chain and the ability to navigate both European and Asian markets with ease. Rather than simply adapting, we’re leveraging this context to strengthen our role as a bridge between East and West. This helps our partners mitigate risk, optimize logistics, and maintain stability in an otherwise volatile global environment.”

The above experts are some of the speakers at the first vertical session organized by pv magazine. Tickets for the Milan conference are available at a 20% discount with code 7600199855.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.